Economic Policy Council Report 2025

Preface

The Economic Policy Council was established in January 2014 to provide independent evaluation of economic policy in Finland. According to the government decree (61/2014), the Council is tasked with evaluating:

- the appropriateness of economic policy goals;

- whether the goals have been achieved and whether the means to achieve the policy goals have been appropriate;

- the quality of the forecasting and assessment methods used in policy planning;

- coordination of different aspects of economic policy and how they relate to other social policies;

- the success of economic policy, especially with respect to economic growth and stability, employment, and the long-term sustainability of public finances;

- the appropriateness of economic policy institutions and structures of public finances.

The Council is appointed by the government based on a proposal by economics departments of Finnish universities and the Academy of Finland. The composition of the Council follows a rotating schedule, and each member serves a four-year term. Council members participate in the Council’s work alongside their regular duties.

In our previous annual report, we assessed the implementation of the consolidation measures outlined in the government programme and the new measures decided by the government in 2024 aimed at strengthening public finances. We also described the rules governing the funding of wellbeing services counties and assessed the financial situation of the counties.

In this report, we focus in particular on the new measures decided by the government in 2025. One area of attention is the decisions made at the government’s mid-term policy session concerning earned income and corporate taxation. We also examine, as a special theme, the Finnish public sector balance sheet and net wealth, taking into account, for example, earnings-related pension funds and the liabilities associated with accrued earnings-related pensions. In this context, we also discuss the government’s preliminary proposal for reforming the earnings-related pension system, published in December. The reform would direct a larger share of public financial assets held in earnings-related pension funds towards equities and potentially other relatively high-risk, high-expected-return investments. We also examine recent developments in the finances of wellbeing services counties and problems related to the determination of service need in the counties.

We do not, of course, comment on all economic policy decisions made by the government in 2025. For example, we do not assess the measures decided or outlined at the government’s mid-term policy session to improve the operating conditions for growth companies. The impact of individual measures is likely to be relatively small, and many of the measures listed at the spending limits session still require further preparation before potential implementation. If realised, however, these measures may together have significant effects.

At the end of 2025, the Council was assigned new tasks under the new Act on the Management of Public Finances. This report has been prepared under the Council’s previous mandate.

The Council relies primarily on forecasts from the Ministry of Finance and does not produce its own economic forecasts. The latest publication used in this report is the Ministry of Finance’s Winter 2025 forecast, published in December 2025.

The Economic Policy Council also commissions external research to support its work. Background reports are prepared and published as supplementary material to the main report. The views expressed in the background reports do not necessarily reflect those of the Council. In connection with this year’s report, a background report by Juha-Matti Tauriainen on the net wealth of general government has been published. The study provides an accessible introduction to the key concepts relating to general government net wealth and a description of the developments in the main items of the Finnish general government balance sheet in the 2000s.

A number of experts have shared their views and expertise with the Council. We thank Tuukka Holster, Lauri Kajanoja, Jussi Kiviluoto, Filip Kjellberg, Konsta Lavaste, Jukka Mattila, Juri Matinheikki, Julia Niemeläinen, Seppo Orjasniemi, Marja Paavonen, Fransiska Pukander, Jenni Pääkkönen, Tanja Rantanen, Ismo Risku, Veliarvo Tamminen, Reetta Varjonen-Ollus and Antti Väisänen for their valuable discussions and for responding to numerous detailed questions.

The annual report of the Economic Policy Council was first published in Finnish. This document is an unofficial English translation based on a machine translation produced with Claude Opus (version 4.6).

Helsinki, 2 February 2026

Niku Määttänen, Chair

Tuukka Saarimaa, Vice-Chair

Liisa Häikiö

Johanna Wallenius

Juha Junttila

Jenni Jaakkola, Secretary General

Henri Keränen, Researcher

Contents

2 Recent economic developments

2.1 Economic growth

2.2 Inflation and interest rates

2.3 Labour markets

2.4 Council views

3 Finances of the wellbeing services counties

3.1 Financial situation of the wellbeing services counties in 2025

3.2 Extension of the deficit-covering period

3.3 Needs-based allocation of funding

3.4 Government targets for the wellbeing services counties

3.5 On the incentives in the funding model

3.6 Council views

4 The Finnish public sector balance sheet

4.1 Balance sheet items and net wealth of the public sector

4.2 Pension reform

4.3 Liabilities associated with publicly subsidised housing production

4.4 Additional withdrawal from the State Pension Fund

4.5 Council views

5 Tax structure

5.1 New tax decisions

5.2 Effects of tax changes on tax bases and aggregate output

5.3 Council views

6 State of public finances and the fiscal stance

6.1 Overview of the government’s fiscal policy plan for 2024–2027

6.2 State of public finances

6.3 Fiscal stance

6.4 Reform of the fiscal policy act

6.5 Council views

References

1 Summary

Recent economic developments

Economic activity has remained subdued throughout the current government term, as measured by both employment and GDP growth. Forecasts for economic growth in 2025 were also revised downwards repeatedly during the year.

At the beginning of the government term, the weak performance was driven in particular by the rapid decline in housing construction that began in 2022. Although the contraction in construction has since levelled off, the volume of construction activity remains very low compared to the situation a few years ago.

The pronounced volatility of construction amplifies cyclical fluctuations in the broader economy and leads to a waste of resources, as a significant share of construction sector workers are periodically unemployed. Going forward, efforts should be made to smooth construction volatility, for example by scheduling public construction projects more countercyclically and by ensuring a steady disposal of city-owned plots for construction in growth centres, allowing plot prices to adjust flexibly in line with demand. At the same time, a requirement should be imposed that construction on allocated plots is not deferred.

Over the past year, economic growth has also been dampened by the rise in the household savings rate and the tightening of fiscal policy. These have reduced domestic demand at a time when output is constrained by insufficient demand relative to productive capacity.

The increase in the household savings rate is not necessarily detrimental to longer-term economic development. It has turned the current account into a slight surplus, meaning that the Finnish economy as a whole is saving. This can be seen as a natural way for the national economy to prepare for foreseeable pressures on public expenditure related to population ageing and the deterioration of the security environment.

Over the longer term, output and employment can grow as exports expand. However, the reallocation of labour from the domestic market sector to export industries takes time. Improved employment through stronger exports also requires sufficiently strong cost competitiveness.

Finances of the wellbeing services counties

The combined finances of the wellbeing services counties (WSCs) were clearly in deficit in 2023 and 2024. In 2025, their finances turned to surplus. This positive development reflects both an increase in WSC funding through the so-called ex-post adjustment and expenditure growth remaining at a moderate level.

However, the deficits in 2023 and 2024 were so large that, taken together, the WSCs still had approximately EUR 2 billion in accumulated deficit at the end of 2025. Under the original rules, this should be covered by corresponding surpluses by the end of 2026. Based on the 2025 financial statement forecasts, it appears that only a few WSCs will be able to meet the original obligation to cover their deficits without substantial additional spending cuts in 2026. On the other hand, accumulating the required surpluses would allow many counties to rapidly increase expenditure again in 2027.

The government has decided to grant some of the counties one or two additional years to cover their deficits. This extension allows for a more even distribution of spending cuts over the coming years and need not increase the aggregate expenditure of the WSCs in the near term.

The obligation to cover deficits continues to compel most counties to contain expenditure growth relative to funding growth, at least in the near term. By contrast, counties that manage to cover their deficits by the end of this year have no comparable incentive to contain expenditure growth. Since the counties do not have the right to levy taxes, they cannot pass on spending cuts to residents in the form of lower taxation. Moreover, expenditure growth in surplus counties will, through the ex-post adjustment, increase the funding of all counties with a lag. In developing the funding model, particular attention should be paid to how the incentives for these counties to improve their operational efficiency or to prioritise their services could be strengthened.

Central government funding of the WSCs should ideally reflect regional service need as accurately as possible. A substantial share of county funding is determined on the basis of diagnosis data collected from the counties. This is underpinned by a model maintained by the Finnish Institute for Health and Welfare (THL), in which individual-level service need is statistically explained by various need factors covering a wide range of morbidity data based on healthcare diagnosis records. The estimated service needs of individuals residing in different counties are then aggregated into county-level service need. However, this constitutes a zero-sum game from the counties’ perspective: a higher estimated service need in one county reduces the funding of the others.

Diagnosis recording practices have varied across counties. This has undermined the alignment of funding with actual service need and has created difficult uncertainty for the WSCs regarding their future funding. Diagnosis-based funding also creates a financial incentive to record certain types of diagnoses with a low threshold and, conversely, to economise on preventive services.

These problems could be significantly alleviated by discontinuing the use of morbidity data in the allocation of funding between counties. Although morbidity data are a good predictor of individual-level service need, calculations by THL suggest that their contribution to estimating county-level service need is very limited. County-level service need could be calculated more simply on the basis of population structure and certain socioeconomic factors.

Public sector balance sheet

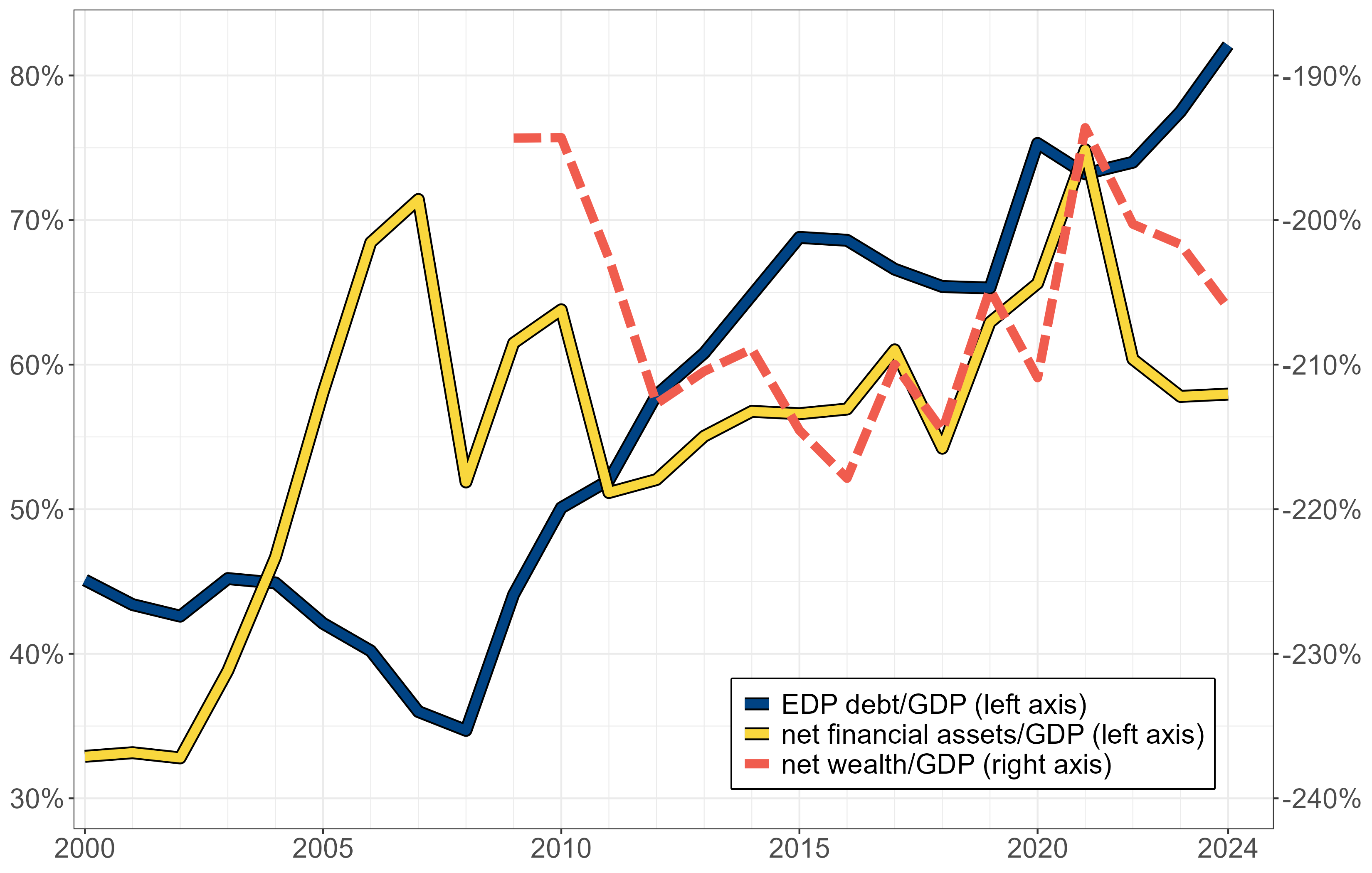

Finland’s general government has both debt and assets. A large share of the financial assets of the public sector consists of investment assets in the earnings-related pension system. Including earnings-related pension assets, Finland’s public sector holds more financial assets than financial liabilities. In other words, the net financial assets of general government — the difference between financial assets and liabilities — are positive. On the other hand, in an even broader examination of the public sector balance sheet, accrued pension entitlements are also counted among the liabilities of the public sector. Their value clearly exceeds the value of the pension funds.

The additional withdrawal of EUR 1 billion from the State Pension Fund to the 2027 central government budget, decided by the government in spring 2025, is an example of a measure that reduces public debt but does not, at least in expected value terms, improve the sustainability of public finances. This is well illustrated by the broader examination of the public sector balance sheet, as the measure does not directly affect the net wealth of the public sector.

Nor is the additional withdrawal of major significance in the overall context of public finances: it marginally reduces both financial assets and future investment returns, as well as the servicing costs of public debt. In addition, it is likely to reduce the volatility of net financial assets by lowering the fluctuation of the market value of financial assets.

It would, however, be desirable for such measures to rest on a predictable and clearly defined plan for managing public sector debts and assets. The same applies, for example, to financing public investments through proceeds from the sale of government equity holdings. The one-off additional withdrawal from the State Pension Fund decided by the government clearly does not represent such an approach.

The government set out in its programme the objective of a pension reform that would strengthen public finances over the long term and stabilise the development of the earnings-related pension contribution through a rules-based stabilisation mechanism. The government published a draft proposal for the reform in December 2025.

The most important element of the reform concerns the investment regulation of private earnings-related pension providers. The reform directs providers to increase their investment risk, for example by raising the share of equities in their overall investment portfolios. To compensate for higher risk, higher investment returns can be expected. The reform also strengthens the funding of the earnings-related pension system by slightly increasing the pre-funding of pensions and by cutting pension index increases in situations where consumer price inflation exceeds the growth of nominal wages for an extended period.

According to the Ministry of Finance, the reform would strengthen public finances, as measured by the sustainability gap, by approximately 0.8 per cent relative to GDP. The effect arises primarily from the increase in investment risk and pre-funding. As a result, the earnings-related pension contribution can probably be lowered in the future compared to a scenario without the reform. A lower pension contribution, in turn, creates room to raise other taxes without increasing the overall tax burden.

The Ministry of Finance’s estimate is based on an analysis examining a large number of different paths or scenarios in which the investment returns of earnings-related pension assets evolve in different ways. The impact assessment for public finances is the median of the sustainability gap effects calculated across these paths — that is, the middle value when ranked by magnitude. The median effect is positive (the sustainability gap narrows), as the reform lowers the earnings-related pension contribution on most paths.

The effect that strengthens public finances materialises only over a very long time horizon. Furthermore, the estimated effect depends on the assumption that, as the earnings-related pension contribution decreases, other taxation will eventually be tightened correspondingly. In addition, the reform slightly increases the uncertainty associated with the sustainability of public finances, as the variation in the earnings-related pension contribution across different paths grows.

Short-term fluctuations in investment returns do not generally pose particular problems for the earnings-related pension system. The system also allows, at least in principle, for the sharing of risks associated with longer-term variation in returns even across generations. It may therefore be entirely reasonable to pursue higher investment returns by accepting greater investment risk.

It is, however, regrettable that the reform did not include an agreement on how increased investment risks are to be shared among employees, retirees, and members of different generations. The current system rests on the premise that, ultimately, the earnings-related pension contribution adjusts if long-term investment returns deviate from expectations. This leaves the investment risks entirely on the shoulders of employees. A significant increase in the pension contribution may not even be a credible option, as it would have adverse repercussions for the rest of public finances.

The government has already decided on a number of cuts to social security benefits. These have, however, mainly targeted income transfers paid to the working-age population. Against this background, it is difficult to justify why pensions, which account for a very large share of all public income transfers, were largely excluded from cuts in the reform. In light of the government’s stated objectives, it would be warranted to re-examine in particular those pension benefits that are not accrued through work but that are also not clearly targeted at low-income individuals.

Developing the social security system coherently is also difficult if various pension benefits are not critically assessed alongside other benefits. For example, eliminating the pension accrual from earnings-related unemployment periods would likely be a preferable option from the perspective of most unemployed individuals compared to the cuts to unemployment benefits already implemented by the government. Income transfers are generally most valuable for wellbeing when individuals have no other income.

Cutting certain pension benefits would also make it possible to lower the earnings-related pension contribution or other social security contributions immediately, and to increase earned income taxation, for instance, without raising the overall tax burden. Unlike the pension reform now proposed, such a package of measures would help slow the pace of public debt accumulation immediately. This would not necessarily require interfering with already accrued pensions.

Tax structure

At the mid-term policy session in spring 2025, the government decided on fairly significant changes to taxation. Earned income taxation will be reduced, particularly in the highest income brackets but also for middle-income earners, starting from 2026, and the corporate tax rate will be lowered by two percentage points from 2027. In addition, the government decided to reduce VAT on food slightly and to raise the inheritance tax threshold. The combined impact of the tax cuts on public revenue is, on a static estimate, approximately EUR 1.3 billion in 2026 and EUR 2.3 billion in 2027.

The government also decided on tax increases totalling approximately EUR 430 million. The government is raising excise duties on tobacco, alcohol, and soft drinks, among other things, and will abolish the tax deductibility of trade union membership fees.

The rationale behind these tax decisions reflects an aspiration to make the tax system more efficient in the sense that it would cause less distortion to earned income, investment, and aggregate output. Based on the research literature, reducing the top marginal tax rate on earned income in particular can be justified on these grounds. Lowering the corporate tax rate may also be sensible from this perspective.

Taken as a whole, however, the tax decisions do not enhance the efficiency of the tax system in a particularly coherent manner. For example, the previous level of earned income taxation for middle-income earners was hardly among the most harmful elements of the tax system in terms of tax efficiency or aggregate output.

From the perspective of strengthening public finances, it would also have been warranted to raise certain taxes that can be considered less harmful than average for aggregate output growth. This would have ensured that the combined effect of the tax decisions does not weaken public finances. For instance, reforming the dividend taxation of unlisted companies or reducing certain business subsidies granted in the form of tax reliefs would have been consistent measures also from the standpoint of tax efficiency.

State of public finances and the fiscal stance

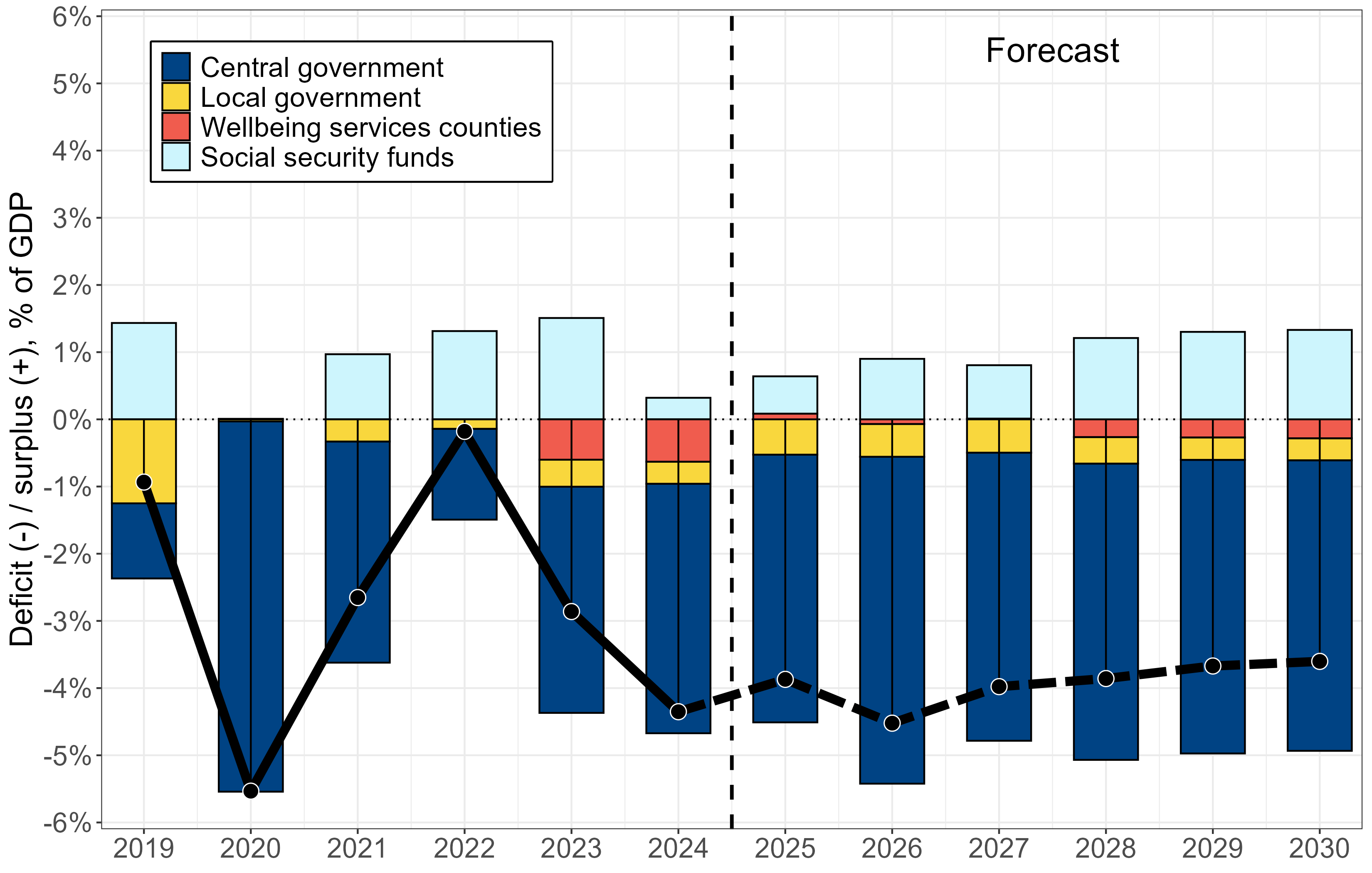

The government does not appear to be on track to achieve its key objectives for strengthening public finances during the current government term. According to forecasts, the growth of the debt-to-GDP ratio will not turn as described in the government programme, and the general government deficit in particular is likely to remain clearly larger than the target set out in the programme.

One key reason for falling short of the targets is that some of the consolidation measures set out in the government programme were uncertain in their effects from the outset. For example, the government aimed for significant spending cuts through productivity-enhancing measures in the WSCs, even though it is in practice difficult to verify whether such improvements actually translate into savings for public finances. A second reason is weaker-than-expected cyclical developments, which have directly increased the deficit and diminished the impact of measures aimed at boosting employment. The growth of interest and defence expenditure also increases the general government deficit significantly compared to the previous government term.

Following the tax decisions made in spring 2025, the fiscal stance in 2026 is not set to tighten materially compared to 2025. This can be considered justified from a cyclical policy perspective, as the rise in unemployment suggests that the economy has unused potential output. However, permanent tax cuts are not a particularly appropriate instrument for managing aggregate demand, as they affect the fiscal position permanently.

The government’s measures as a whole, including those decided earlier, are nevertheless likely to strengthen public finances significantly compared to a scenario without them. Their impact on the annual deficit can be expected to grow over time. It takes time for the economy to adjust to the weakening of domestic demand caused by spending cuts or tax increases. It is also clear that, regardless of the cyclical conditions, not all public sector workers displaced as a result of consolidation measures will be immediately absorbed by the private sector.

The near-term outlook for public finances also includes positive factors: for example, the increase in household savings and growth in the labour force may bolster economic growth in the near term in various ways. Nevertheless, balancing public finances will require significant consolidation measures in future government terms.

2 Recent economic developments

2.1 Economic growth

Revisions to growth forecasts

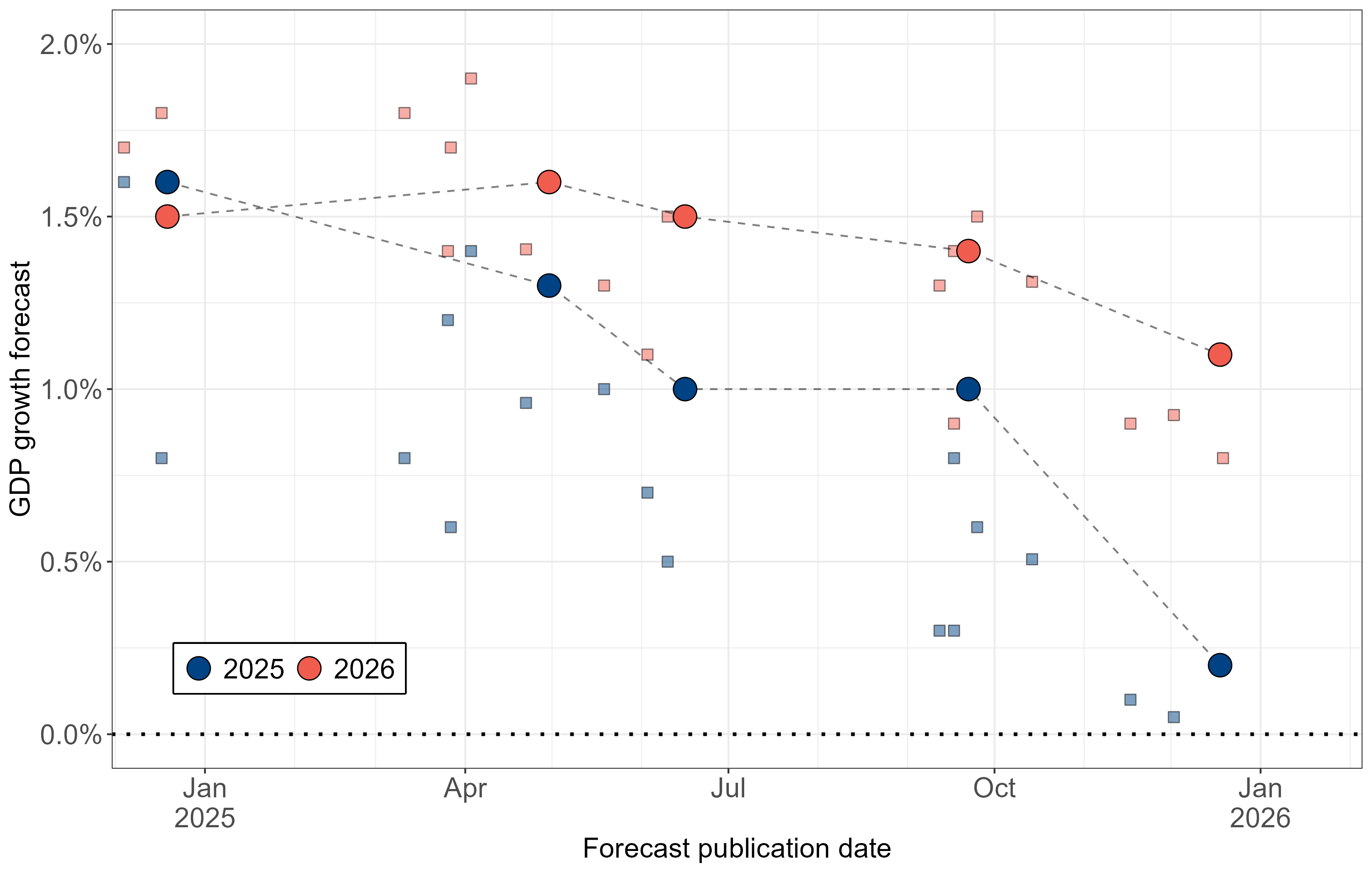

Economic growth in 2025 was weaker than generally anticipated. This is also evident in Figure 2.1.1, which presents GDP growth forecasts for 2025 and 2026 published between the end of 2024 and during 2025, ordered by their publication date. Forecasts for 2025 were revised markedly downwards over the course of the year: at the beginning of the year, economic growth of approximately 1.5 per cent was still expected, but by the end of the year the forecasts pointed to growth close to zero. Forecasts for 2026 have also been revised downwards on average during the year, but considerably less so than those for 2025.

Notes: Ministry of Finance forecasts are represented by larger dots and connected by dashed lines. The other forecasting institutions included are: Bank of Finland, European Commission, IMF, OECD, Labore, Etla and PTT.

The figure separately identifies the Ministry of Finance forecasts for 2025 and 2026, on which the government relies when planning its fiscal policy. Over the course of the year, the Ministry of Finance forecasts for GDP growth in 2025 were more optimistic than most other forecasts published at roughly the same time, although the most recent forecast published in December 2025 no longer differed materially from the others. With respect to the growth forecast for 2026, no systematic difference relative to other forecasting institutions is discernible, at least not very clearly.

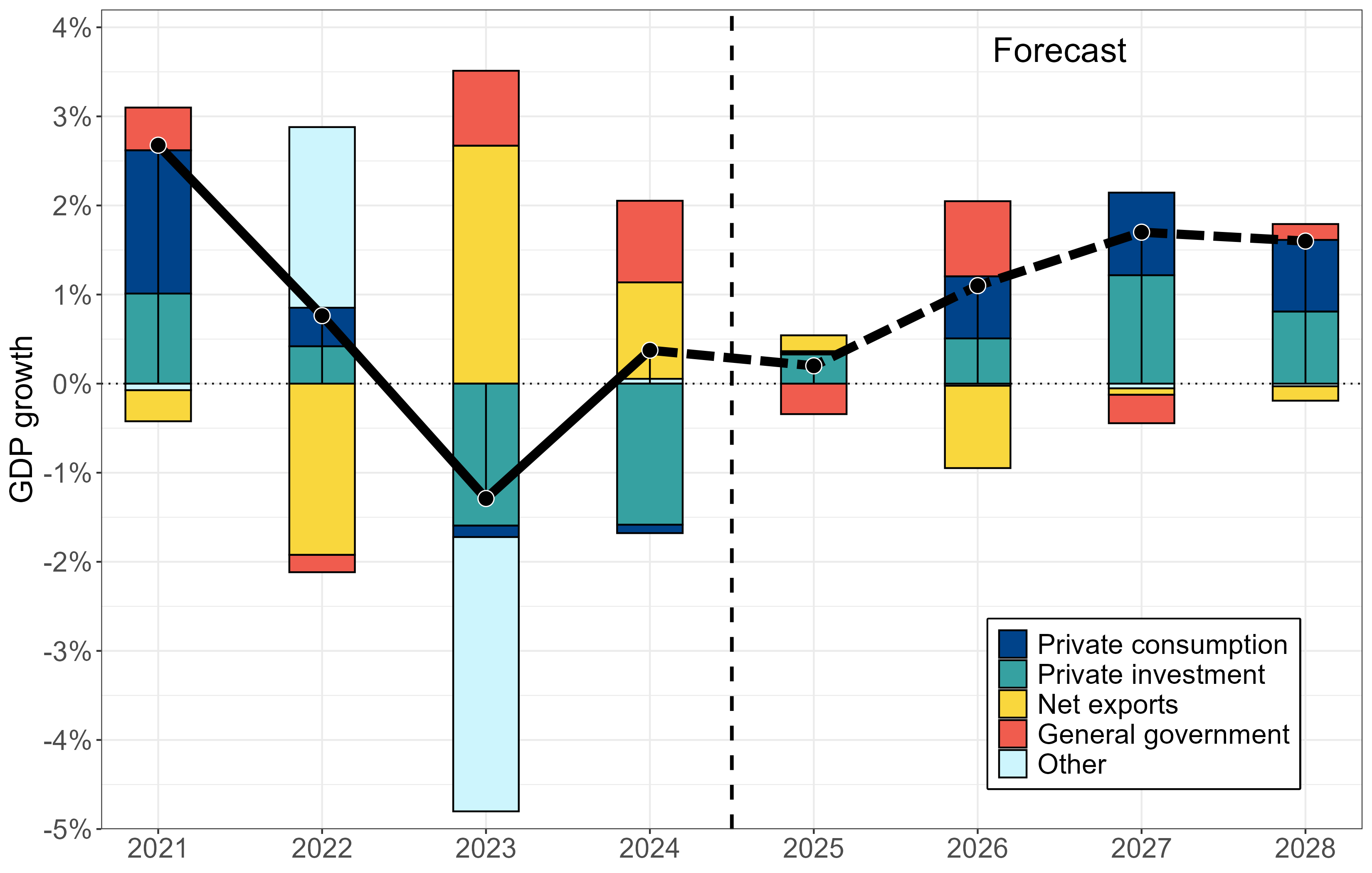

Figure 2.1.2 shows the contributions of different demand components to annual real GDP growth in 2021–2024 and, based on the Ministry of Finance forecast, in 2025–2028. In recent years, net exports and general government have contributed positively to GDP growth, whereas private consumption and, in particular, private investment have contracted in real terms.

The following subsections describe in more detail recent developments and the outlook for private consumption, investment, and exports and imports. Changes related to general government are discussed in greater detail in the chapter on the government’s fiscal policy (Chapter 6).

Source: Statistics Finland, Ministry of Finance (2025f).

Domestic consumption demand

Private consumption declined in real terms in 2023 and 2024. This is visible in Figure 2.1.2 as a small negative growth contribution from private consumption. The Ministry of Finance estimates that the volume of private consumption in 2025 remained at the previous year’s level (Ministry of Finance, 2025f), implying a zero growth contribution. At the same time, however, household disposable income has grown in recent years in both nominal and real terms.

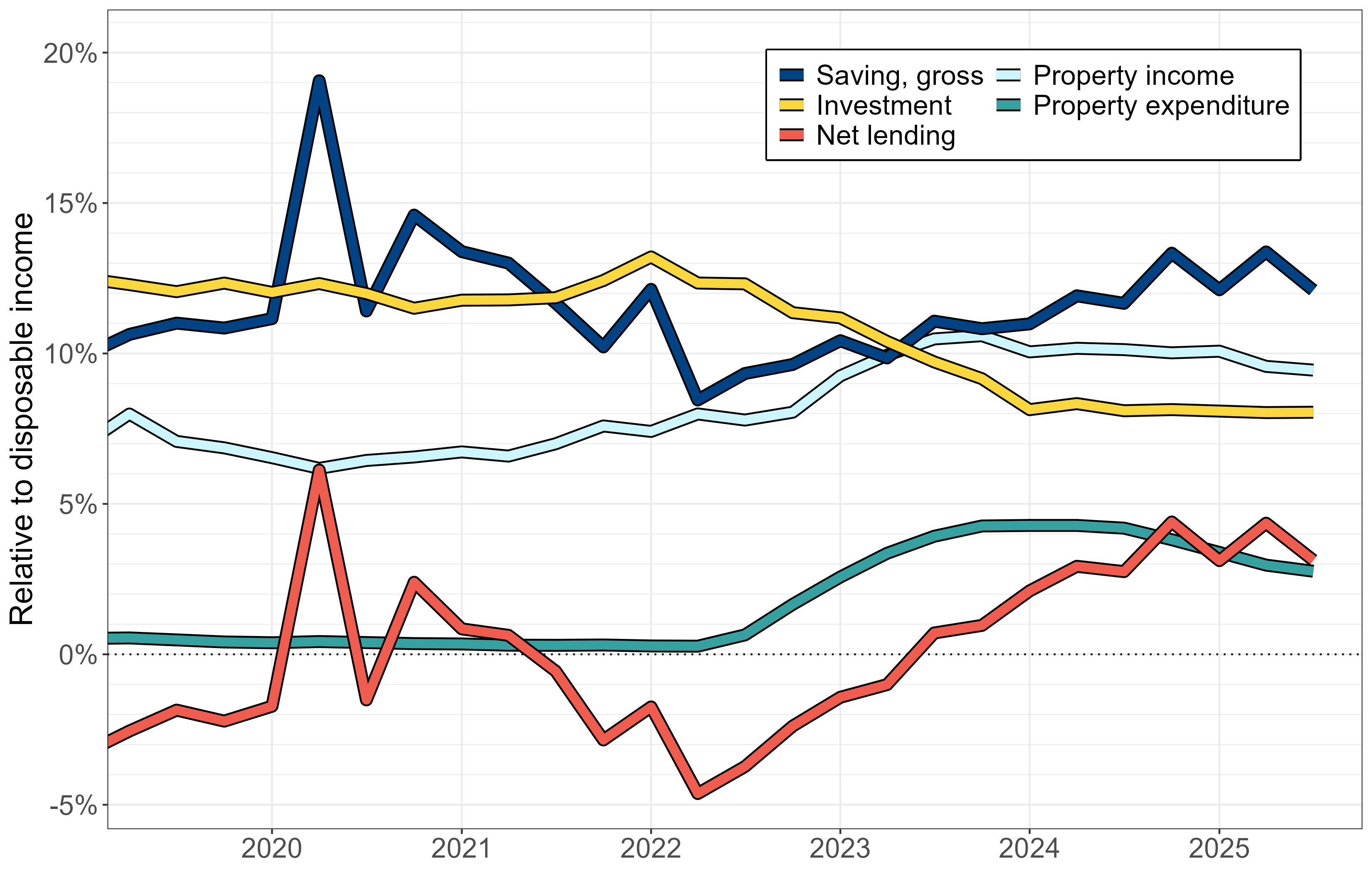

Figure 2.1.3 depicts household saving, investment, net lending, and property income and expenditure relative to disposable income. By definition, gross saving is the difference between disposable income and individual consumption expenditure. Expressing this difference as a ratio to disposable income yields the gross savings rate.1 The figure shows that the gross savings rate began to rise during 2022. Households have thus been consuming a smaller share of their disposable income, which partly explains the subdued growth in private consumption in 2023–2025.

Source: Statistics Finland.

Figure 2.1.3 also shows that the ratio of household investment to disposable income (the investment rate) began to decline at the same time as the savings rate started to rise. This development has been reflected in the housing market, as household investment is predominantly directed towards housing.

The simultaneous increase in saving and decrease in investment have also marked a turning point in household indebtedness. The difference between the gross savings rate and the investment rate described above roughly corresponds to household net lending relative to disposable income. Figure 2.1.3 shows that, as the savings rate rose and the investment rate declined from 2022 onwards, household net lending has turned positive. In 2022, household net lending stood at approximately \(-\)4.5 billion euros, whereas by 2024 it was roughly the same amount in positive territory. The household debt-to-income ratio has accordingly begun to decline.2

These changes in household saving and investment behaviour have clearly reduced aggregate demand. The shift in the savings and investment rates coincided with the year 2022, when interest rates rose markedly from the previous near-zero level. The rise in interest rates may have altered household behaviour both by changing the attractiveness of saving or borrowing and by affecting household income and expenditure. The impact of higher interest rates is illustrated in Figure 2.1.3 particularly by the pronounced increase in property expenditure, which consists mainly of mortgage costs. On the other hand, household property income grew almost simultaneously. The increase in property income was, however, smaller than the increase in property expenditure.

The effects of higher interest rates vary considerably across households. For example, households whose wealth is predominantly in owner-occupied housing and who carry large mortgage debt are likely to have responded to higher interest rates differently from households with little or no debt who instead earn interest income. In addition to higher interest rates, many other factors may also underlie the changes in household saving behaviour, such as increased unemployment risk.

According to the Ministry of Finance forecast, private consumption will return to growth in 2026–2028 (Ministry of Finance, 2025f). In 2026, the volume of private consumption is forecast to grow by 1.4 per cent. Since the projected growth in consumption is nearly as rapid as the projected growth in household real disposable income (1.2 per cent), the household savings rate is not expected to change significantly. In subsequent forecast years, consumption growth would outpace income growth, implying a gradual decline in the savings rate from its current level.

Investment

The sharp contraction in private investment in 2023 and 2024 clearly weighed on aggregate output growth. In both years, private investment declined by approximately 8 per cent from the previous year. According to the Ministry of Finance forecast, private investment growth turned positive again in 2025, with investment increasing by 1.9 per cent compared to the previous year. The forecast projects that private investment growth will continue in the coming years, reaching its strongest pace in 2027, when growth is expected to be nearly 7 per cent. At that point, private investment growth would account for a significant share of aggregate output growth from the demand-side perspective (Figure 2.1.2).

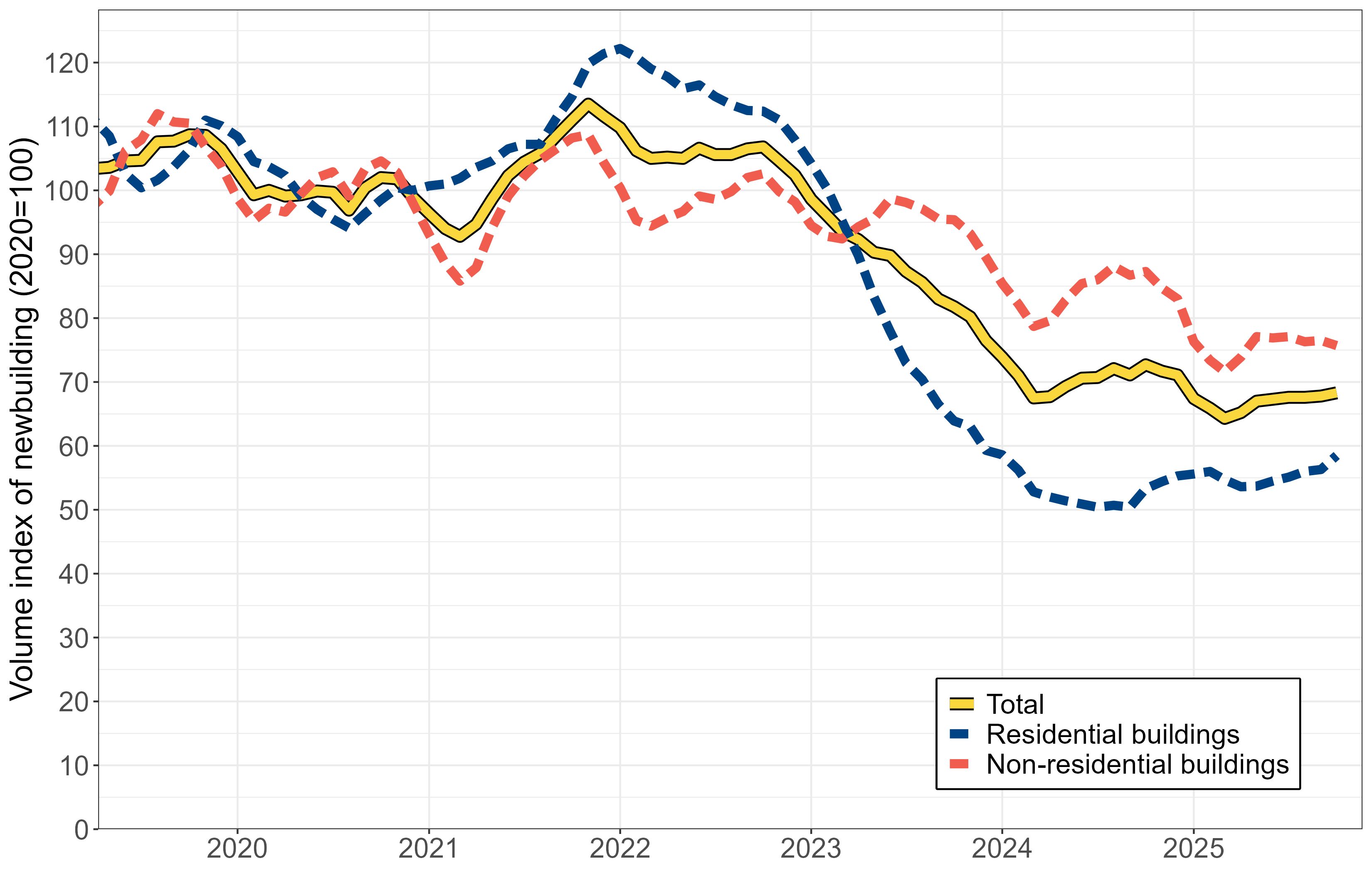

The contraction in private investment in 2023 and 2024 was particularly linked to the collapse in residential construction. Figure 2.1.4 shows that the volume of new construction turned into a steep decline at the end of 2022, especially in the case of residential buildings. This turning point coincides with the rise in the general level of interest rates (see the following subsection). Based on the figure, the volume of new residential construction has roughly halved from its 2022 level.

Source: Statistics Finland.

Residential construction includes renovation construction in addition to new construction. Although renovation construction has also declined, the decrease has been smaller than in new construction (Ministry of Finance, 2025d). Overall, residential construction investment has contracted by approximately one third from its 2022 level (Ministry of Finance, 2025f). This has undoubtedly had a major impact on the economy, as the share of residential construction in total investment was nearly one third in 2022.

According to the Ministry of Finance forecast, residential construction grew by 0.5 per cent in 2025. In 2026, the volume of residential construction is forecast to grow by 6 per cent, and in 2027 by 7 per cent.

Investment in machinery and equipment has not experienced a comparable collapse to that in construction. Investment in machinery and equipment declined by approximately 4 per cent in 2023 but grew by nearly 5 per cent the following year. In 2025, investment in machinery and equipment grew by around one per cent according to the Ministry of Finance forecast. In 2026, machinery and equipment investment will be boosted by the commencement of F-35 fighter jet deliveries, and total growth is forecast to be 13.5 per cent, partly on account of this. The fighter jet procurement is reflected in a sharp increase in public investment: public investment is forecast to rise by as much as 22 per cent in 2026, while private investment growth is forecast at 2.8 per cent (Ministry of Finance, 2025f). Investment growth is projected to exceed aggregate output growth over the entire forecast horizon.

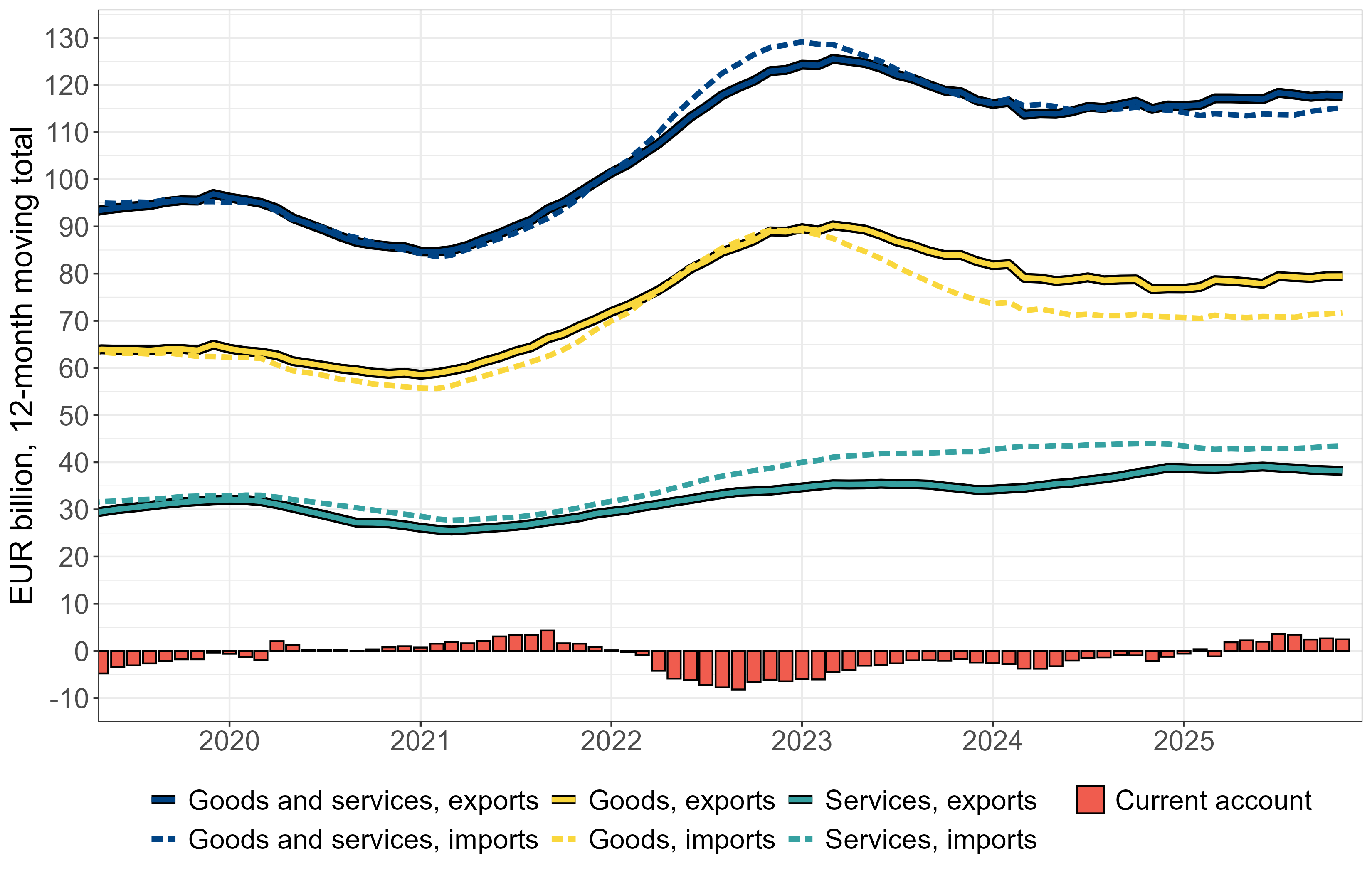

Exports and imports

In recent years, net exports have contributed positively to GDP growth (Figure 2.1.2). However, the increase in net exports, particularly in 2023, was due to a contraction in imports rather than growth in exports, as both exports and imports declined from the previous year. Based on Figure 2.1.5, both exports and imports remain below their 2022 levels in current prices, but the contraction in imports has been considerably larger than that in exports.

Source: Statistics Finland.

In 2024, exports grew thanks to an increase in services exports. According to the Ministry of Finance forecast, the volume of exports grew by 1.8 per cent in 2024 and by 2.4 per cent in 2025. The volume of imports, by contrast, declined in 2024, with growth at \(-\)0.8 per cent. In 2025, the Ministry of Finance estimates that imports grew by 2 per cent (Ministry of Finance, 2025f).

When comparing changes in the volume of exports and imports with Figure 2.1.5, it should be noted that both export and import prices declined in 2024 and 2025. This means that the nominal developments shown in the figure do not directly reflect changes in export or import volumes. Finland’s terms of trade — the ratio of export prices to import prices — have been influenced in recent years in part by changes in energy prices. The terms of trade deteriorated in 2022, for example, as a result of the sharp rise in (imported) energy prices.

As exports have come to exceed imports, Finland’s current account also turned into surplus in 2025. A surplus on the current account means that the national economy as a whole is not accumulating debt to the rest of the world. The Ministry of Finance estimates that the current account surplus stood at 0.3 per cent of GDP in 2025, but forecasts that it will swing back into a roughly equivalent deficit in the near term. The forecast projects that both export and import volumes will grow in 2026–2028, but that import volumes will grow faster than exports (Ministry of Finance, 2025f).

Box 2.1. On US trade policy

The trade policy of the new US administration caused considerable turmoil in the spring of 2025. At the outset of Trump’s second term, tariffs were initially raised on products imported from Canada, Mexico and China, as well as on steel, aluminium and the automotive industry. At the same time, the administration was preparing a broader shift in trade policy. Uncertainty about the content of the new trade policy and the motives behind it pushed indices measuring policy uncertainty to historically high levels in the spring of 2025 (see e.g. Gensler et al. (2025)).

In early April 2025, the Trump administration launched so-called reciprocal tariffs, under which the tariffs imposed on imports from different countries would be determined by the size of the US trade deficit with each country. The stated minimum tariff level was, however, 10 per cent, applicable also to countries with which the United States runs a trade surplus. The proposed tariff levels were considerably higher than expected, and financial markets reacted strongly in the week following the announcement. The Trump administration soon decided on a 90-day pause on the reciprocal tariffs while maintaining the 10 per cent minimum tariff level. A brief trade-war-like situation also developed between China and the United States, with both sides raising trade barriers in turn. Subsequently, however, tariffs between the two countries also settled at lower levels.

These so-called reciprocal tariffs were ultimately applied in the late summer. Following the launch of the new tariff policy, the US administration has, however, agreed on lower import tariffs with several trading partners. These agreements may have stipulated lower tariffs conditional on certain other policy objectives being advanced. For example, the agreement with the EU, which set a tariff ceiling of 15 per cent with some exceptions, stipulated that the EU would not levy tariffs on US products and that EU member states would purchase large quantities of liquefied natural gas from the United States.

Despite these trade agreements, there remain uncertainties regarding the stability of the tariffs. First, there is significant legal uncertainty surrounding the implementation of tariff policy. Under US law, the authority to regulate foreign trade and impose tariffs rests primarily with Congress, not the President. The Trump administration has justified its sweeping tariff increases by invoking exception statutes previously enacted by Congress that grant the President powers to intervene in trade on grounds such as national security or unfair trade practices. The matter is pending before the Supreme Court, but no binding precedent has yet been established. Due to the slow pace of legal proceedings, the tariffs remain in force and payable even though their legality continues to be contested.

The Trump administration has also demonstrated a willingness to deviate from established trade agreements and to use tariff threats as an aggressive negotiating tactic. The most recent example is the diplomatic dispute over the status of Greenland, which threatened to jeopardise the trade agreement negotiated with the EU. The United States threatened to impose an additional 10 per cent tariff from February 2026 on countries — Finland included — deemed to be obstructing its objectives. The situation, however, appeared to dissipate as quickly as it arose, as only a few days later Trump announced the withdrawal of the immediate tariff threat, reportedly following the emergence of a preliminary understanding on an Arctic agreement. This episode underscores the unpredictability of Trump’s trade policy: tariff policy can change with a single social media post.

As a consequence of Trump’s second-term trade policy, US tariff levels in 2025 were higher than at any point since the 1940s. At the beginning of 2026, US consumers were estimated to face an average effective import tariff of approximately 17 per cent (Yale Budget Lab, 2026).

Import tariffs are fundamentally a tax that creates a wedge between the price paid by the domestic buyer and the price received by the foreign seller. As such, they distort the global division of labour and lead to a less efficient allocation of economic resources than would prevail in the absence of tariffs. For the country imposing the tariffs, they constitute a negative supply shock; for other countries, they are primarily a negative demand shock. However, in a situation where countries face tariffs of different magnitudes, domestic industry may benefit from its own country’s import tariffs. On the other hand, with globalisation, the economy and its production chains have become increasingly complex, and even the industry of the tariff-imposing country is readily harmed by tariffs if it uses imported intermediate inputs in its production.

In addition to the effects described above, the uncertainty associated with trade policy is also likely to reduce investment. One mechanism is related to the fact that investments are often irreversible. If the profitability of an investment project depends on trade policy and there is substantial uncertainty about future policy, it may be worthwhile to defer the investment decision until the uncertainty clears. There is also empirical evidence of the negative impact of trade policy uncertainty on investment; see for example Caldara et al. (2020).

As a small open economy, Finland is exposed to uncertainty related to trade policy. Although the majority of Finland’s foreign trade takes place within the EU internal market, the United States accounted for approximately 10 per cent of Finland’s goods exports in 2024, with the value of goods exports to the United States amounting to approximately 8.1 billion euros. Finland’s trade balance with the United States was also strongly in surplus, with the value of goods imports standing at approximately 3 billion euros in 2024.a

The economic impact of the tariffs is mitigated by the fact that services are excluded from tariffs. Finland’s services exports to the United States amounted to approximately 6.1 billion euros in 2024, and services imports to approximately 5 billion euros.

The effects of US tariff policy on the Finnish economy have been assessed ex ante by, among others, Juvonen et al. (2024), Ali-Yrkkö (2025) and Silvo and Juvonen (2025). Assessing the effects ex ante is, however, challenging, as every modelling exercise must be based on certain assumptions about the eventual conditions of the trade policy landscape and the durability of higher tariffs. The models also differ in terms of which effects they aim to capture. The above-mentioned assessments assumed tariff rates of 10–25 per cent on Finnish exports. The estimated GDP impact in these assessments ranges roughly from \(-\)0.5 per cent to \(-\)1.6 per cent.

2.2 Inflation and interest rates

Inflation

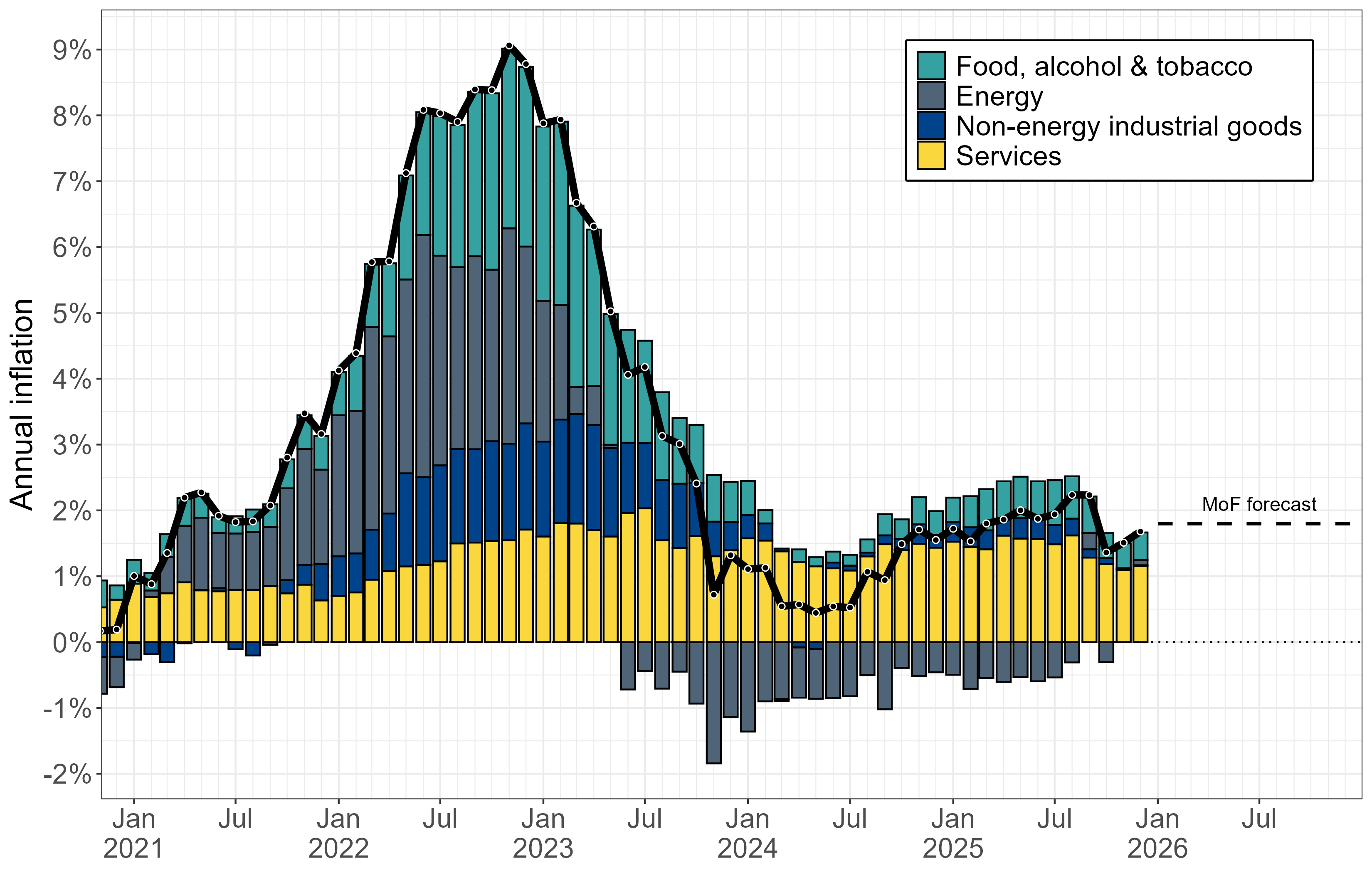

Inflation as measured by the Harmonised Index of Consumer Prices (HICP), which captures inflation excluding the impact of interest expenses, stood at approximately 1.8 per cent in 2025. According to the decomposition in Figure 2.2.1, the main upward driver of inflation has been the rise in services prices. Energy prices have, by contrast, continued to slightly dampen inflation. The Ministry of Finance forecasts a similar inflationary path going forward: the HICP is projected to rise by 1.8 per cent also in 2026 and 2027 (Ministry of Finance, 2025f).

Source: Statistics Finland, Ministry of Finance (2025f).

Notes: The bars represent the contributions of different consumption categories to overall inflation,

shown by the black line. The dashed line represents the Ministry of Finance forecast for the full year

2026.

Interest rate developments

During 2025, the ECB lowered its key policy rate from 3 per cent at the beginning of the year to 2 per cent. The last rate change took place in June. Euro area inflation has recently been close to the 2 per cent target, so there is no immediate pressure to ease or tighten monetary policy in this regard. Based on market interest rates in January 2026, the next rate change is expected to be a rate increase rather than a rate cut.

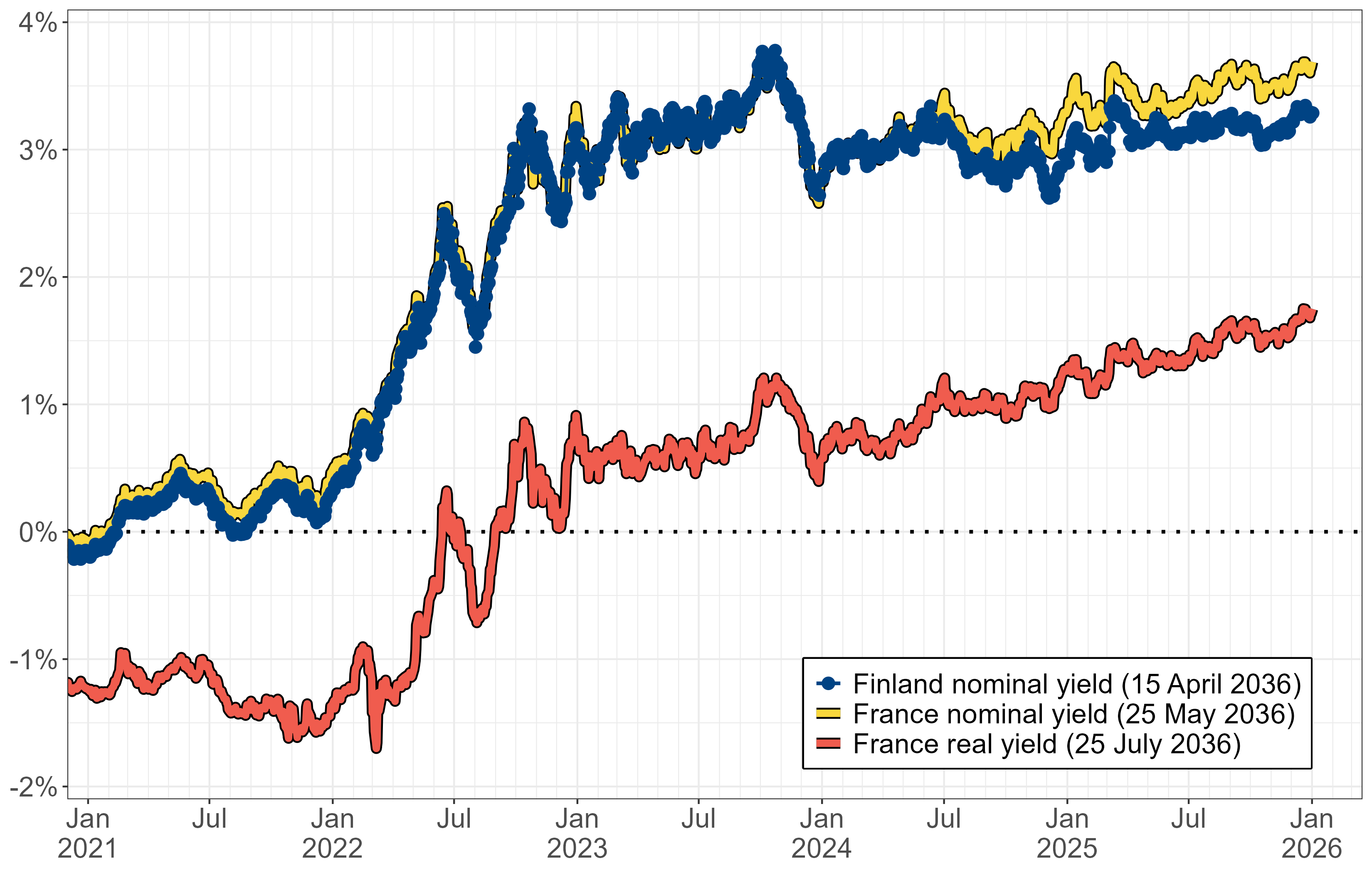

Figure 2.2.2 shows the yield developments of selected Finnish and French government bonds maturing in 2036 over the past five years. For France, the figure depicts the development of both the nominal and the real yield. The real interest rate refers to the nominal interest rate adjusted for inflation. It is a more important price than the nominal rate when considering, for example, the economic incentive to save or the burden that public debt servicing places on public finances. The real yield is derived from the secondary market prices of inflation-linked French government bonds indexed to the euro area consumer price index. For Finland, the figure shows only the yield on a nominal government bond of corresponding maturity, as Finland has not issued inflation-linked government bonds.

Source: Bank of Finland, Agence France Trésor (Bloomberg).

Notes: The maturity date of the bond is shown in parentheses. The French real yield is for an OAT€i bond

indexed to the euro area Harmonised Index of Consumer Prices.

Although a small gap has opened between Finnish and French nominal government bond yields over the past year, the overall development of yields has been sufficiently similar to justify the assumption that the real yield on French government bonds is fairly close to the real interest rate that investors would, in expected value terms, require to lend to the Finnish government.

The real yield on French government bonds rose slightly during 2025, standing at approximately 1.5 per cent at year-end. For Finland, the real yield can be estimated to have risen somewhat less over the same period, as the nominal yield on French government bonds has risen above that of Finnish bonds. In any case, the substantial rise in the real interest rate that occurred in 2022 appears to have been permanent, at least for the time being. This makes the servicing of public debt considerably more expensive than before (see EPC (2024), Chapter 2.4).

2.3 Labour markets

Unemployment

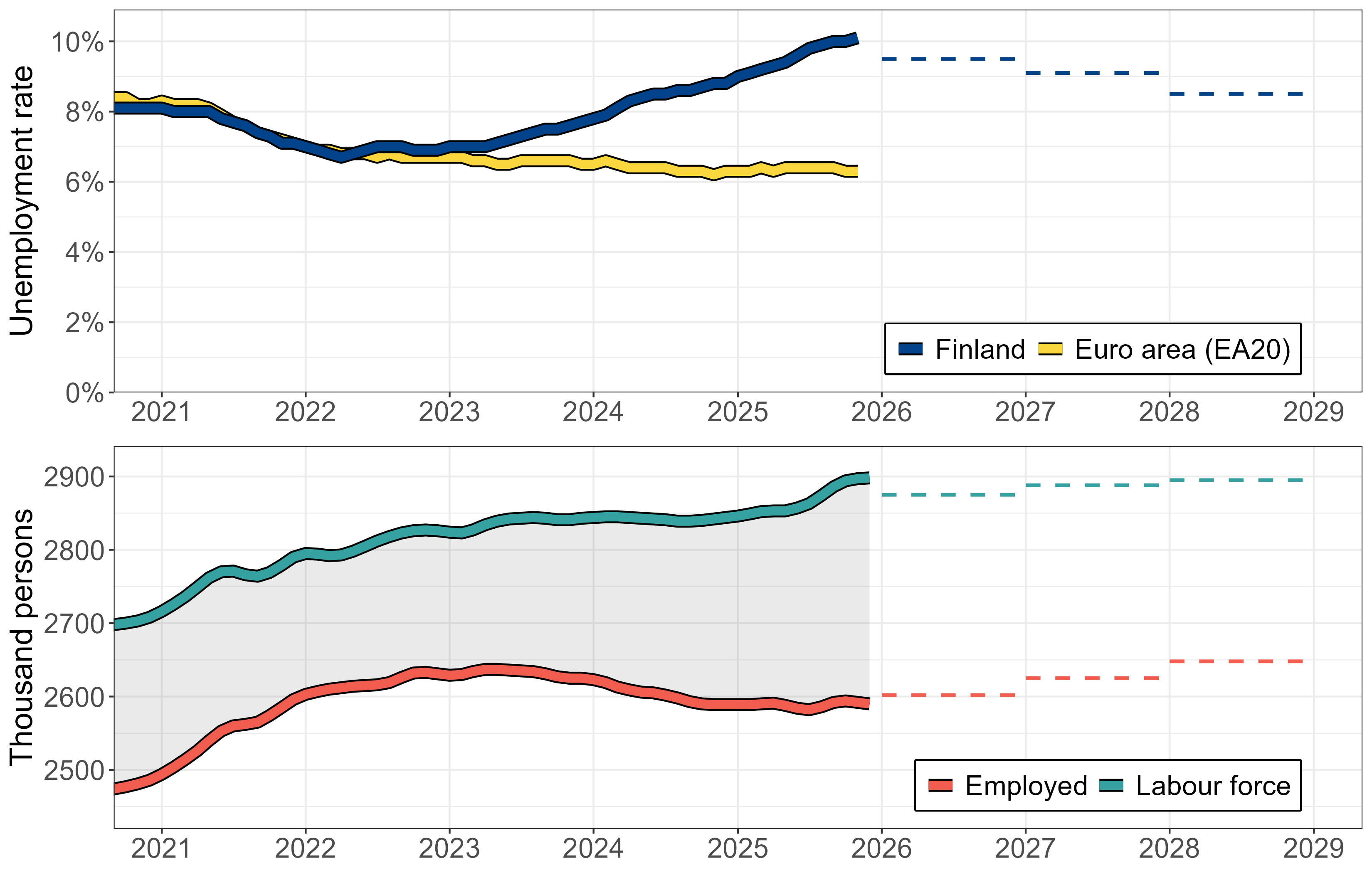

The unemployment rate based on Statistics Finland’s Labour Force Survey has been rising in Finland since 2022. In 2022, the unemployment rate in the 15–74 age group was 6.8 per cent, compared to 9.7 per cent in 2025. The upper panel of Figure 2.3.1 compares the trend in the unemployment rate in Finland and the euro area, based on Eurostat data. In 2021 and 2022, unemployment rate developments were still very similar, but since then Finland’s unemployment rate has embarked on an upward trajectory while the euro area rate has continued on a gently declining trend. According to the Ministry of Finance forecast, Finland’s unemployment rate will remain elevated in the near term, still standing at 9.5 per cent in 2026 (Ministry of Finance, 2025f). The Ministry of Finance forecasts for the different years are shown by dashed lines in the figure.

Source: Eurostat, Statistics Finland, Ministry of Finance (2025f).

Notes: Ministry of Finance forecasts for the full years 2025–2028 are shown by dashed lines.

The lower panel of Figure 2.3.1 shows separately the trend in the number of employed persons and in the labour force in Finland over the same period, based on Statistics Finland’s Labour Force Survey. The unemployment rate is the difference between the labour force and the number of employed persons (the number of unemployed) divided by the labour force. The figure shows that although the number of employed persons has declined from its 2023 level, the recent increase in unemployment largely reflects growth in the labour force. The labour force grew fairly rapidly, particularly towards the end of 2025. At the same time, the unemployment rate rose even though the number of employed persons changed only marginally. According to the Labour Force Survey, the number of unemployed persons in 2025 was 278 thousand on an annual basis, which is 74 thousand more than in 2023. Over the same period, the labour force grew by 36 thousand and the number of employed persons declined by 38 thousand.

Employment rate

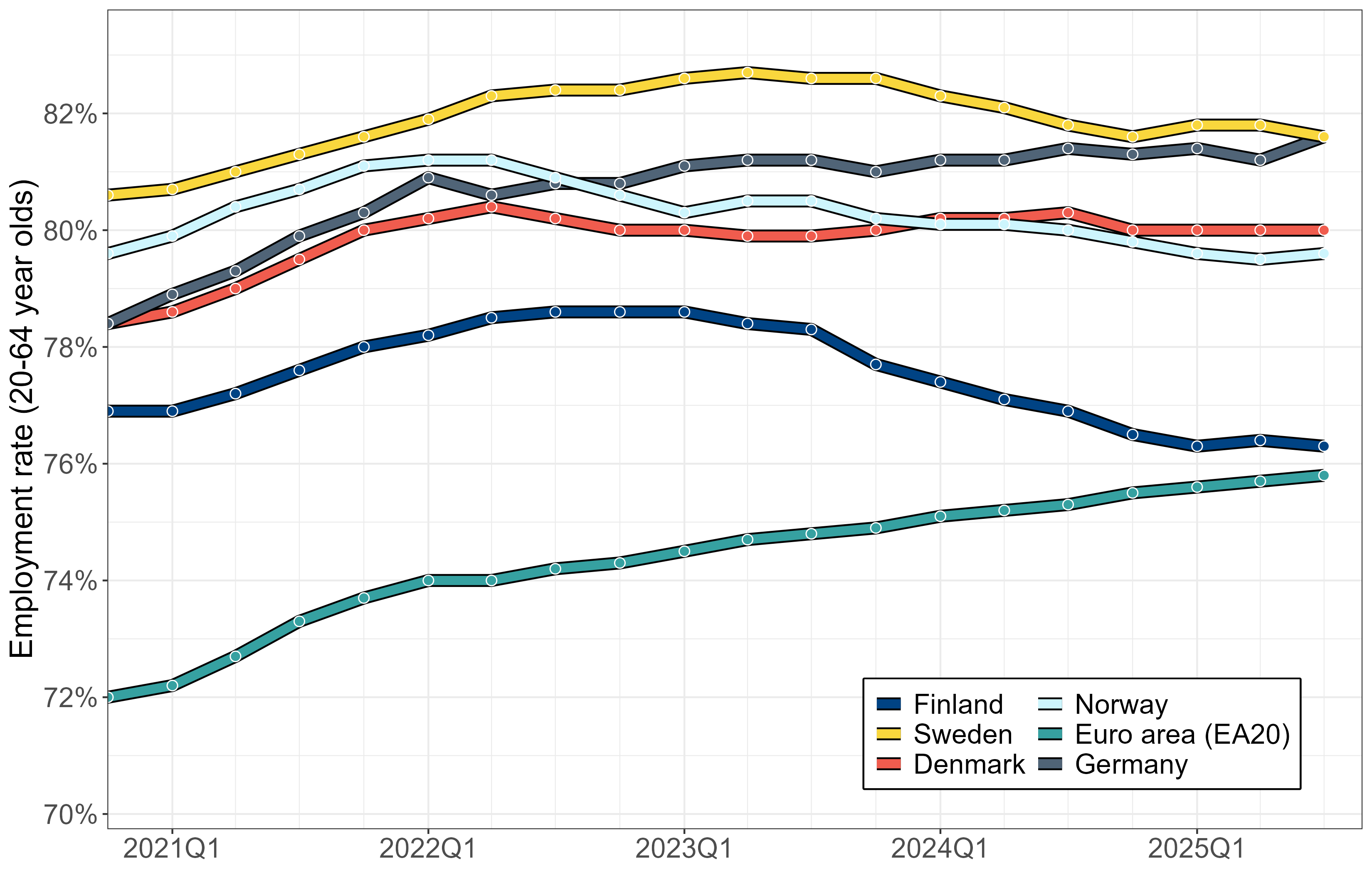

Figure 2.3.2 shows employment rate developments in the 20–64 age group in selected countries, based on Eurostat data. According to Statistics Finland’s Labour Force Survey, the employment rate in this age group was 76 per cent in Finland in 2025, approximately 2 percentage points lower than in 2022, when the employment rate peaked. Although the employment rate in 2025 was lower than in preceding years, the figure suggests that the declining trend in the employment rate appears to have levelled off during 2025.

Source: Eurostat.

Among the countries shown in Figure 2.3.2, the employment rate has also declined slightly in Sweden and Norway, whereas in Denmark and Germany it has remained very stable over the same period. The euro area employment rate has grown steadily and is now close to Finland’s level.

Job vacancies and labour market tightness

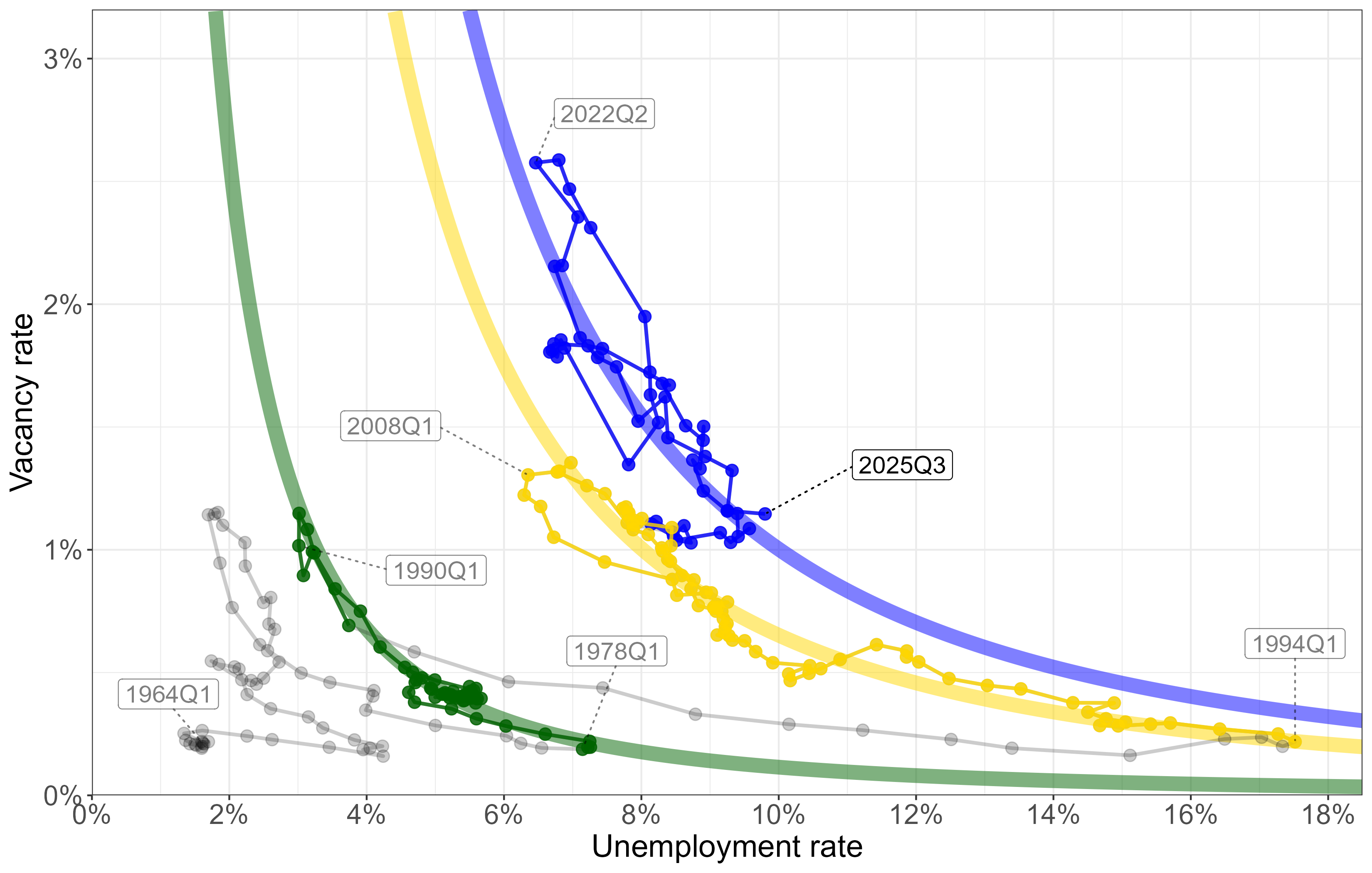

The Beveridge curve describes the relationship between unemployment and job vacancies. (The vacancy rate shown in the figure is the ratio of vacancies to the labour force.) There is typically a negative relationship between the two: during periods of high unemployment, vacancies are few, which is characteristic of a downturn. Conversely, during periods of low unemployment, vacancies are plentiful, which is typical of a boom.

Figure 2.3.3 shows how the unemployment rate and the vacancy rate in Finland have evolved in relation to each other. The differently coloured Beveridge curves in the figure represent periods during which the relationship between unemployment and vacancies has remained relatively stable. These Beveridge curves have, however, shifted outwards when more recent time periods are examined compared to preceding decades. This outward shift means that a given number of vacancies relative to the labour force is typically associated with a higher unemployment rate than before.

Source: Gäddnäs and Keränen (2023), updated with more recent Eurostat data.

Notes: The coloured Beveridge curves represent the average positions of the curves in 1978–1990 (green curve),

1994–2012 (yellow curve) and 2013– (blue curve).

Examining developments in recent years reveals that the tight labour market of 2022 has, by 2025, deteriorated markedly from the perspective of workers. The approximately three-percentage-point increase in the unemployment rate from its 2022 level has been accompanied by a decline in the vacancy rate from approximately 2.5 per cent to slightly above 1 per cent. This development broadly follows the blue Beveridge curve in the figure, suggesting that it reflects a standard cyclical weakening.

2.4 Council views

Economic activity has remained subdued throughout the government term, as measured by both employment and GDP growth. At the beginning of the government term, the weak performance was driven in particular by the rapid decline in housing construction that began as early as 2022.

The pronounced volatility of construction is more broadly harmful to the economy. It amplifies cyclical fluctuations and leads to an inefficient use of resources, as a significant share of construction sector workers are periodically without work. Going forward, efforts should be made to smooth construction volatility, for example by scheduling public construction projects more countercyclically and by promoting steadier private construction activity. This could be supported, for example, by ensuring a more even disposal of city-owned plots for construction over the business cycle and by allowing plot prices to adjust flexibly in line with demand.

The rise in the household savings rate has also weighed on economic growth in recent years. It has reduced domestic demand at a time when output is constrained to some extent by insufficient aggregate demand relative to productive capacity. The weak cyclical situation has also likely amplified the short-term adverse effects of the government’s consolidation measures, described in Chapter 6, on output and employment through the aggregate demand channel.

The increase in the household savings rate is not necessarily detrimental to longer-term economic development. It has already turned Finland’s current account from a small deficit into a small surplus, meaning that the Finnish economy as a whole is saving. This can be seen as a natural way of preparing for foreseeable expenditure pressures, such as the growth in care expenditure associated with population ageing and the need to increase defence spending in response to the deteriorated security environment.

Output and employment can grow through exports rather than domestic demand. However, the reallocation of labour from the domestic market sector to export industries takes time. Improved employment through stronger export demand also requires sufficiently strong cost competitiveness.

The unemployment rate has risen to a very high level compared to recent years. At the same time, however, the labour force has grown markedly. The growth of the labour force is a positive development from the perspective of future economic growth. It means that labour shortages will not immediately become a constraint on growth as the economy recovers.

3 Finances of the wellbeing services counties

In our previous annual report, we described the funding model for the wellbeing services counties (WSCs), the state of their finances in 2023 and 2024, and the challenges arising from the obligation to cover deficits. In this chapter, we assess the financial situation of the WSCs in 2025 and their near-term outlook, based on the data reported by the counties in early autumn 2025. In addition, we examine the assessment of service need, which is central to the funding of the counties and the problems associated with its application. Finally, we assess the savings targets set by the government for the WSCs and progress towards meeting them.

The wellbeing services counties reported their 2025 financial statement estimates at the end of January 2026. Based on the updated data, the combined 2025 result at the national level would be better than the forecast data suggested.3 The update does not materially change the overall picture of WSC finances presented in this chapter, but the divergence between counties appears to be intensifying.

3.1 Financial situation of the wellbeing services counties in 2025

After two years of significant deficits, the combined finances of the wellbeing services counties are turning to a slight surplus in 2025. Based on the financial statement forecasts, the WSCs would have a combined surplus of approximately EUR 200 million in 2025. This considerable improvement in the financial situation is primarily explained by the EUR 1.4 billion ex-post adjustment added to funding in 2025 and by expenditure growth remaining at a moderate level of approximately 3 per cent.

Despite the surplus result in 2025, the wellbeing services counties have a total of EUR 2.2 billion in accumulated deficit. The accumulated deficit is primarily attributable to the rapid growth in expenditure in 2023.4 Although expenditure growth slowed markedly already in 2024, the finances of the WSCs were still significantly in deficit that year, as the level of WSC funding is adjusted through the ex-post adjustment to match realised expenditure only with a two-year lag. At the national level, funding in 2024 was approximately EUR 400 million, or approximately 2 per cent, less than realised expenditure in 2023.

The purpose of the ex-post adjustment is to ensure that realised expenditure does not diverge from funding at the national level and that the WSCs thereby have the means to carry out their assigned tasks.5 However, the restoration of balance in WSC finances as measured by the deficit alone is not sufficient: under current legislation, the deficit accumulated in 2023 and thereafter must be covered by corresponding surpluses by the end of 2026.6

Financial situation by county

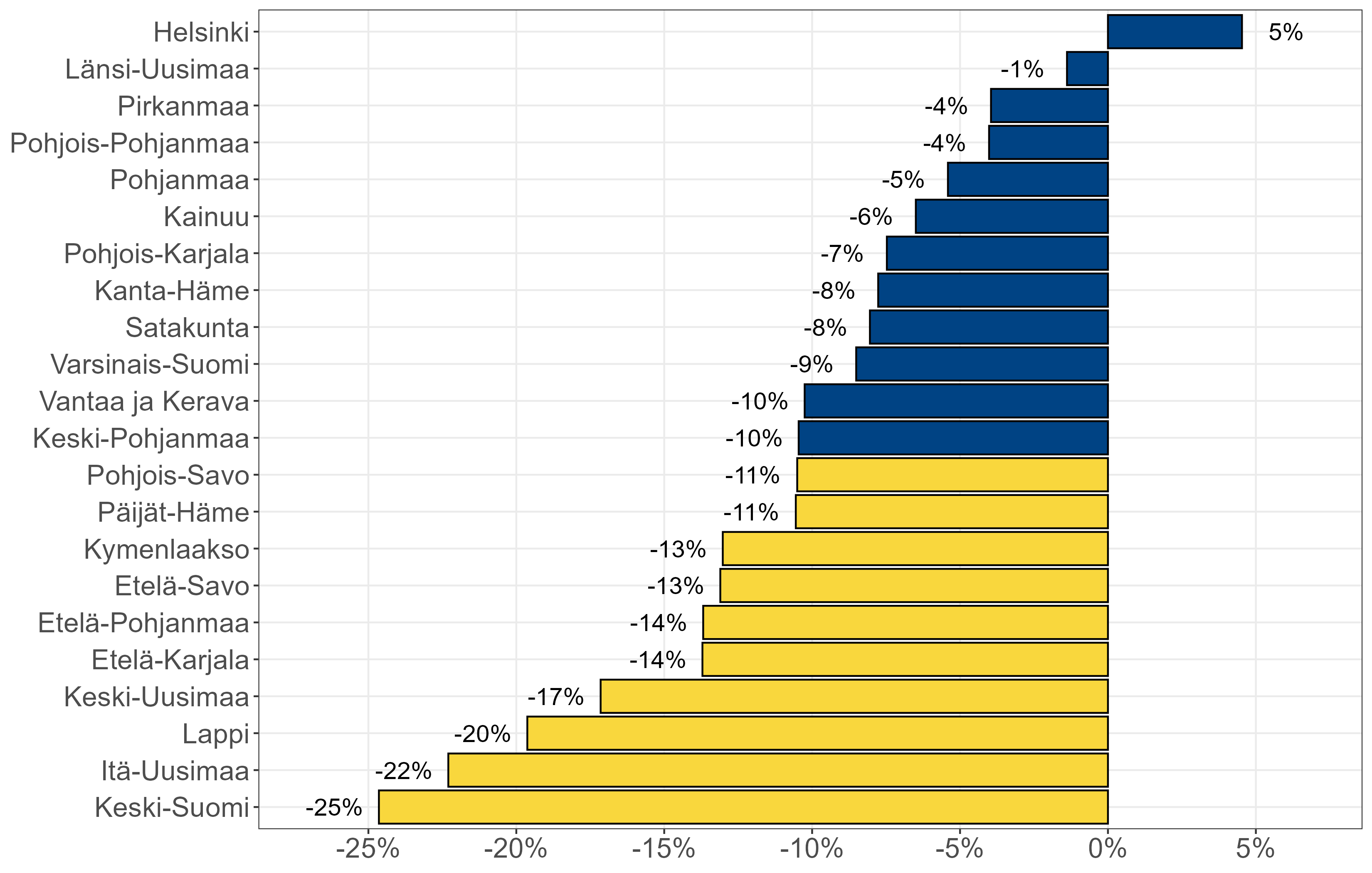

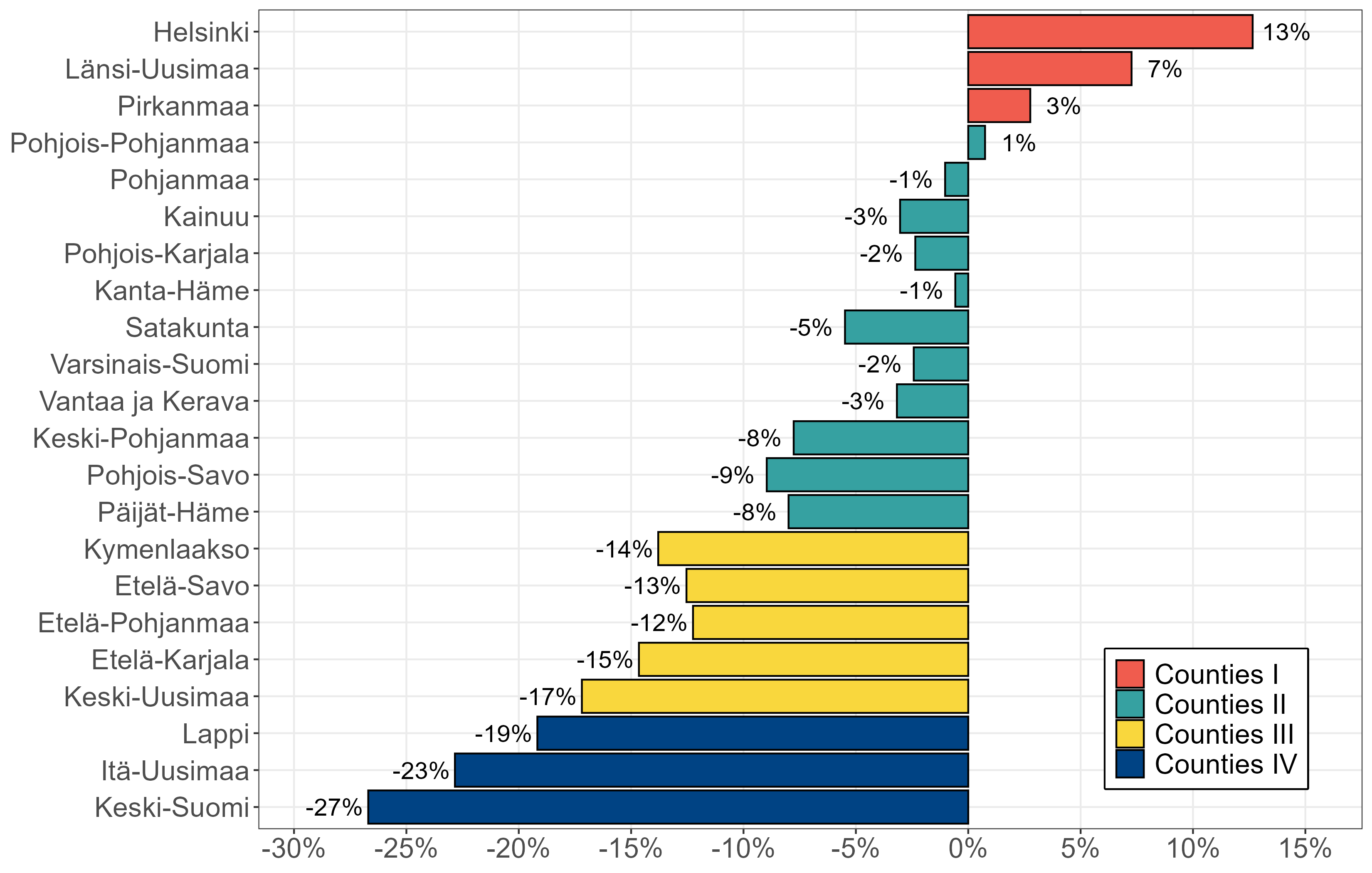

Although the combined finances of the WSCs are turning to a slight surplus, the financial divergence between counties is continuing and intensifying. Despite the moderate growth in expenditure, ten counties remain in deficit in 2025. The ex-post adjustment added to funding in 2025 was allocated to the counties in proportion to their imputed funding, not on the basis of county-specific deficits. This has contributed to the divergence in the financial situation across counties. Figure 3.1.1 shows the accumulated deficit (or, in the case of Helsinki, the accumulated surplus) of each WSC over 2023–2025, relative to county-specific central government funding in 2026. In order to cover their accumulated deficits by the end of 2026, the counties would need to generate surpluses corresponding to the shares of 2026 funding shown in the figure.

Counties marked in blue had a surplus in 2025 based on the financial statement forecasts, while counties marked in yellow were in deficit in 2025. Source: State Treasury, Ministry of Finance, Council’s calculations.

The figure shows that there are significant differences in the financial situation across counties. The City of Helsinki has the strongest financial position. At the end of 2025, it has approximately EUR 140 million in accumulated surplus, corresponding to a surplus of approximately 5 per cent relative to Helsinki’s 2026 funding.

Based on the financial statement forecasts, 11 wellbeing services counties are on track to move from deficit into surplus in 2025. The blue bars in Figure 3.1.1 show, however, that the 2025 surplus is not sufficient in any of these counties (excluding Helsinki) to cover the deficit accumulated in 2023 and 2024. Taking into account the projected 2025 surplus, the remaining deficit to be covered in these counties ranges from 1 to 10 per cent relative to 2026 central government funding. In euro terms, the combined accumulated deficit of these counties stands at EUR 875 million at the end of 2025.

Despite the moderate growth in expenditure, ten counties remain in deficit in 2025 according to the financial statement forecasts (yellow bars in Figure 3.1.1). The combined deficit of these counties over 2023–2025 ranges from 11 to 25 per cent relative to 2026 funding. In euro terms, this group’s accumulated deficit over 2023–2025 totals approximately EUR 1.5 billion. The weakest financial positions are in Keski-Suomi, Itä-Uusimaa and Lappi, all of which have accumulated deficits exceeding 20 per cent relative to their 2026 funding.

Reasons for the financial divergence

The imbalance between funding and expenditure became very significant for several counties already in 2023, as expenditure growth varied between 4 and 17 per cent across counties. Reasons for the differences in expenditure growth across counties included, among others, differences in the initial conditions regarding the integration of services and finances. The baseline year 2022 expenditure data reported by the municipalities contained deficiencies due to municipalities’ incentives to under-budget health and social care expenditure and due to the impact of the COVID-19 pandemic on service provision. In addition, some counties initiated fiscal consolidation already in 2023.

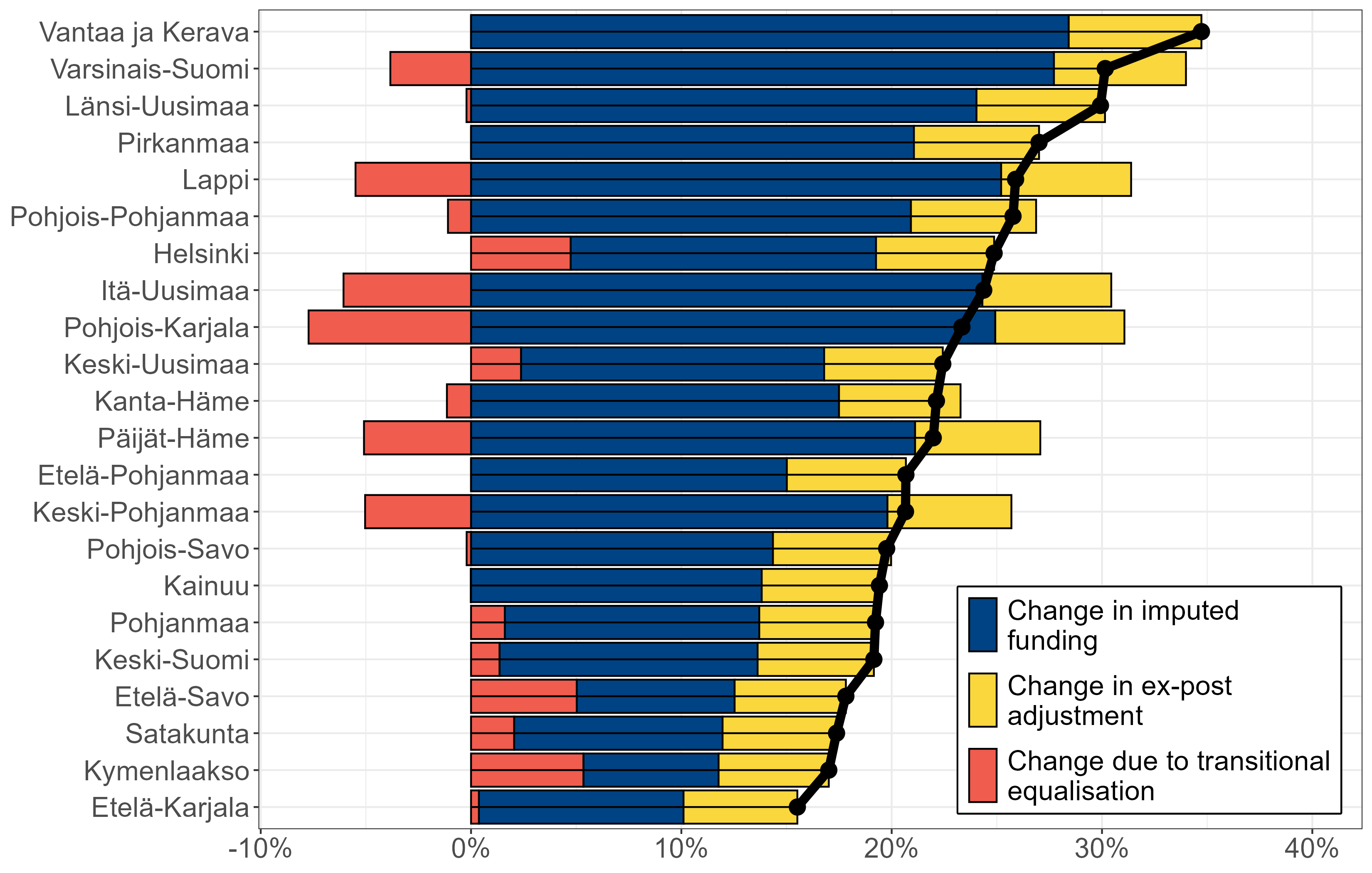

The national level of funding is adjusted annually by the WSC price index, by the estimated growth in service need, by changes in funding corresponding to changes in statutory tasks, and by the ex-post adjustment. The county-specific allocation of funding is also updated annually to reflect changes in population structure, county-specific health and social care service need, and other factors determining the level of funding. In addition, funding is affected by county-specific transitional equalisation additions and deductions. Figure 3.1.2 shows the development of funding over 2022–2026 by county, broken down into changes in imputed funding, the ex-post adjustment, and transitional equalisations.

Black dots represent the total change in funding over 2022–2026. Source: State Treasury, Ministry of Finance, Council’s calculations.

At the national level, WSC funding in 2026 is nominally 24 per cent higher than the amount that municipalities reported spending on the provision of corresponding services in 2022. By county, funding has increased by 16 to 35 per cent compared to the 2022 expenditure of the municipalities in each county’s area. County-specific changes in imputed funding are primarily explained by changes in population and estimated service need.

Figure 3.1.2 also shows the share of the 2025 and 2026 ex-post adjustments in funding. The ex-post adjustment to funding does not reflect county-specific deficits but only the combined expenditure developments of all counties. The figure shows that the funding increase through the ex-post adjustment is roughly proportional for all counties. As a result, Helsinki, which was the only county to record a slight surplus in 2023 and 2024, receives a total of EUR 290 million through the ex-post adjustment in 2025 and 2026. On the other hand, the ex-post adjustment covers only approximately 60 per cent of the 2023 and 2024 deficits of Keski-Suomi, Lappi and Itä-Uusimaa, which are in the weakest financial position. For these counties, the ex-post adjustment falls EUR 225 million short of their combined accumulated deficit.

3.2 Extension of the deficit-covering period

In our previous annual report, we recommended granting additional time for the deficit-covering period, so that counties could spread their expenditure adjustments more evenly over several years. In our assessment, the obligation under existing legislation to cover deficits by the end of 2026 would force many counties first to make very substantial spending cuts, after which they would have the opportunity to increase expenditure rapidly.7

Covering the deficits by the end of 2026 would mean that the WSCs would need to cut their expenditure at the national level by an estimated 4 per cent in nominal terms in 2026 compared to 2025. Figure 3.2.1 shows the county-specific maximum change in expenditure that would allow each county to cover the accumulated deficit shown in Figure 3.1.1 by the end of 2026.

The bars represent the county-specific maximum change in expenditure in 2026 that would allow counties to cover their accumulated deficit by the end of 2026. Counties are ordered according to the accumulated deficit shown in Figure 3.1.1. Classification of counties: I: Counties that are likely to cover their deficits during 2026, and Helsinki. II: Counties with an accumulated deficit of 4–11% relative to 2026 funding. III: Counties with an accumulated deficit of 13–17% relative to 2026 funding. IV: Counties with an accumulated deficit exceeding 20% relative to 2026 funding. Source: State Treasury, Ministry of Finance, Council’s calculations.

The figure shows that for the majority of counties, covering deficits during 2026 would require nominal cuts to expenditure. The required cuts range from 1 to 27 per cent. A few counties would be able to cover their deficits even if expenditure were to increase in nominal terms in 2026. In the case of Helsinki, the maximum change in expenditure shown in the figure would mean that Helsinki would draw down its accumulated surplus and its finances would be in balance at the end of 2026. The figure shows that the scale of the required consolidation or possible expenditure growth does not depend directly on the amount of accumulated deficit at the end of 2025 shown in Figure 3.1.1. The county-specific consolidation requirement is also affected by the timing of consolidation measures already undertaken and by the development of funding.

The government submitted a legislative proposal (HE 189/2025) in late 2025, proposing a temporary amendment to the legislation governing the covering of deficits. Under the proposal, the Ministry of Finance could, upon application by a county, grant an extension of one or two years for covering deficits. Counties could thereby spread the required spending cuts over a maximum of three years.

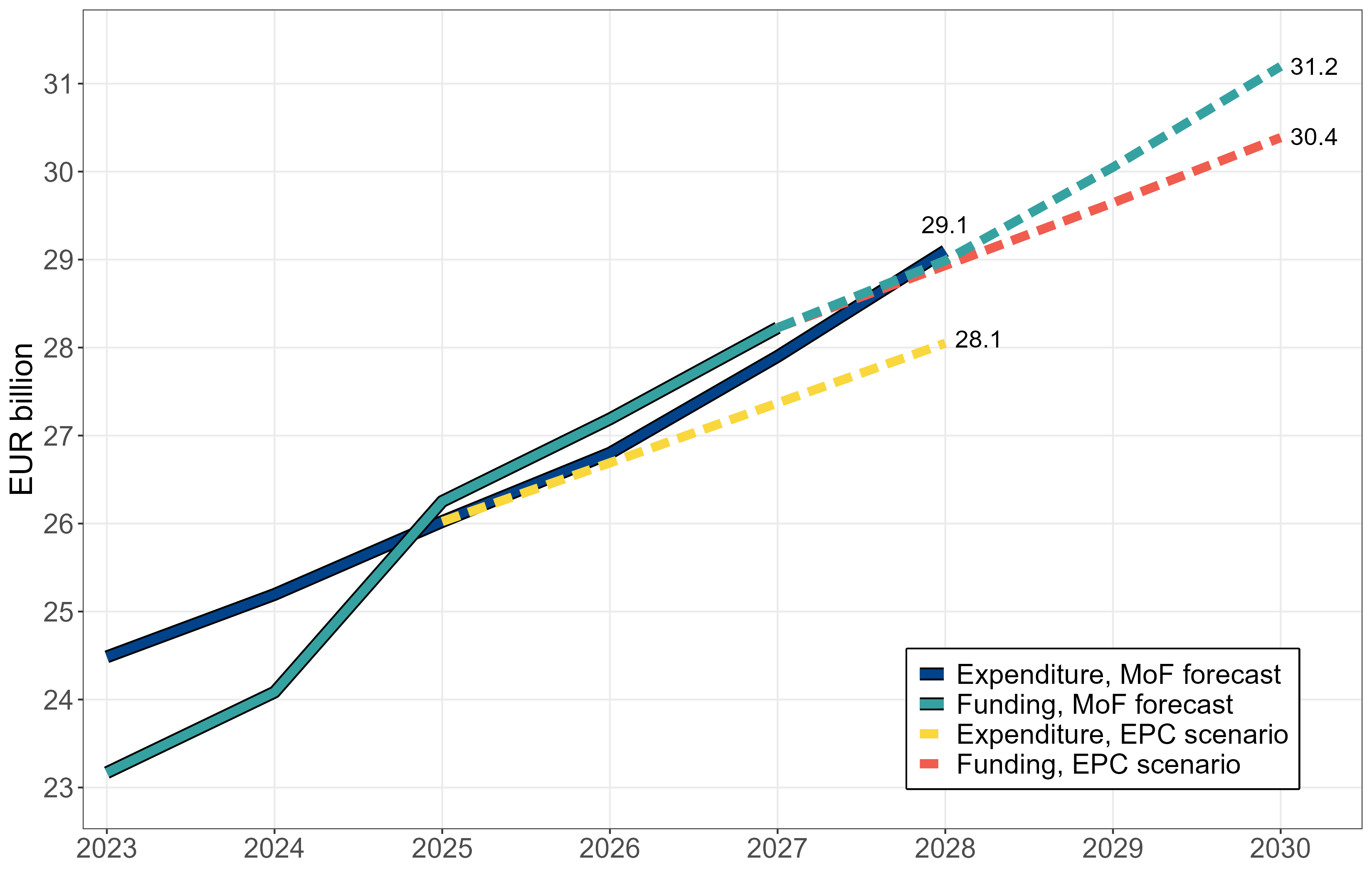

In the Ministry of Finance forecast, the annual growth in WSC expenditure is estimated at approximately 4 per cent in 2026–2028, taking into account the growth in wages in the health and social care sector that exceeds the general increase in the level of earnings.8 The forecast is by nature a pressure calculation, meaning that it does not assume significant consolidation measures by the counties themselves. Figure 3.2.2 shows the expenditure development consistent with the Ministry of Finance forecast for 2026–2028, as well as the development of central government funding in 2028–2030 if expenditure were to develop as forecast. The figure shows that if the Ministry of Finance forecast were to materialise, the WSCs would be only marginally in surplus in 2026–2027 and slightly in deficit again in 2028. In aggregate, the WSCs would still have approximately EUR 1.6 billion in accumulated deficit at the end of 2028.

The blue line shows the combined realised expenditure of the WSCs in 2023–2024, expenditure based on the financial statement forecasts in 2025, and expenditure consistent with the Ministry of Finance forecast for 2026–2028. The solid green line shows central government funding for the WSCs in 2023–2027 based on realised expenditure, and the dashed green line shows central government funding for 2028–2030 if expenditure were to develop in line with the Ministry of Finance forecast. The dashed yellow line shows expenditure development based on the Council’s calculations, in which counties consolidate by a total of EUR 1 billion over 2026–2028, and the dashed red line shows the corresponding development of central government funding in 2028–2030 under this consolidation assumption. Source: Ministry of Finance, Council’s calculations.

Covering the EUR 2.2 billion accumulated deficit in WSC finances with corresponding surpluses by the end of 2028 would require average annual expenditure growth of 2.5 per cent over 2026–2028. This would mean that the annual growth in combined WSC expenditure would be approximately 1.5 percentage points lower than the 4 per cent annual growth in the Ministry of Finance forecast. In euro terms, this would correspond to spending cuts of approximately EUR 1 billion relative to the Ministry of Finance forecast in 2028.

Figure 3.2.2 also shows the development of central government funding resulting from such expenditure development. Lower expenditure growth would generate combined surpluses for the WSCs over 2026–2028. At the same time, it would keep central government funding after 2028 at a lower level than under the Ministry of Finance forecast expenditure path, as the ex-post adjustment that raises funding in line with realised expenditure would be smaller.

Below, we present a simplified calculation of how the approximately EUR 1 billion in expenditure consolidation relative to the Ministry of Finance forecast described above would be distributed across counties, if all counties were granted additional time to cover their deficits until the end of 2028.

Example of the consolidation requirement by county group

In Table 3.2.1, the wellbeing services counties are divided into four groups (I–IV) on the basis of their combined surplus or deficit accumulated over 2023–2025. Column (1) of the table shows the size of each county group measured by its share of total national funding in 2026. Column (2) shows the accumulated deficit in millions of euros over 2023–2025, and column (3) shows the accumulated deficit relative to 2026 funding.

|

| (1) | (2) | (3) | (4) | (5) | |

|

|

Share

of

WSC

finances,

% |

Accumulated

deficit,

EUR

m |

Accumulated

deficit,

% |

Avg.

max.

change

in

expend.,

% |

Total

consol.

by

2028,

EUR

m | |

|

| ||||||

|

| ||||||

| Counties I | 28 | 10 | 0 | 5.0 | +250 | |

| Counties II | 46 | -990 | -8 | 3.0 | -350 | |

| Counties III | 15 | -595 | -14 | 1.0 | -400 | |

| Counties IV | 10 | -625 | -22 | -2.0 | -500 | |

| WSCs total | 100 | -2200 | -8 | 2.5 | -1000 | |

Classification of counties: I: Counties that are likely to cover their deficits during 2026 (Länsi-Uusimaa and Pirkanmaa) and Helsinki. II: Counties with an accumulated deficit of 4–11% relative to 2026 funding (Kainuu, Kanta-Häme, Keski-Pohjanmaa, Pohjanmaa, Pohjois-Karjala, Pohjois-Pohjanmaa, Pohjois-Savo, Päijät-Häme, Satakunta, Vantaa ja Kerava and Varsinais-Suomi). III: Counties with an accumulated deficit of 13–17% relative to 2026 funding (Etelä-Karjala, Etelä-Pohjanmaa, Etelä-Savo, Keski-Uusimaa, Kymenlaakso). IV: Counties with an accumulated deficit exceeding 20% relative to 2026 funding (Itä-Uusimaa, Keski-Suomi and Lappi).

Accumulated deficit, EUR m (2) is calculated using 2023 and 2024 financial statement data and 2025 preliminary financial statement data. Accumulated deficit, % (3) is calculated by dividing (2) by each county’s 2026 funding. Total consolidation by 2028, EUR m in column (5) is calculated on the basis of the difference between the maximum change in expenditure in column (4) and the Ministry of Finance forecast, relative to the 2025 expenditure level of each county group.

Source: State Treasury, Ministry of Finance, Council’s calculations.

The starting assumption of the calculation is that county expenditure would grow at approximately 4 per cent annually in line with the Ministry of Finance forecast, if counties were to undertake no new consolidation measures. County-specific funding is assumed to develop in line with calculations published by the Ministry of Finance.9 In the illustrative calculation, the average annual change in expenditure over 2026–2028 that would allow each county group to just cover its accumulated deficit by the end of 2028 has been computed. This maximum annual average change in expenditure resulting from the obligation to cover deficits is shown in column (4) of the table.

The euro amount in column (5) represents the total required consolidation over 2026–2028 by county group. It is calculated as the difference between the maximum change in expenditure computed for each county group in column (4) and the Ministry of Finance forecast, relative to the combined 2025 expenditure level of each county group.

Column (5) of Table 3.2.1 shows how the combined consolidation of approximately EUR 1 billion at the national level would be distributed across county groups. It should be noted that there is still considerable county-specific variation in accumulated deficits and consolidation pressure within each group. Moreover, the results of the calculation are sensitive to assumptions about the timing of consolidation, as the assumption regarding 2026 consolidation affects 2028 funding through the ex-post adjustment. The illustrative calculation is intended only to provide a rough indication of the scale of consolidation that covering deficits by the end of 2028 would require from different counties.

Counties I: Helsinki has posted a slight surplus already in 2023–2025 (and would therefore already fall outside the scope of the proposed extension regulation). The calculation also assumes that Länsi-Uusimaa and Pirkanmaa will cover their deficits during 2026. The deficit-covering requirements would therefore not bind these three counties in 2027 and 2028. However, the calculation assumes that these three counties would aim to keep their finances in balance in 2027 and 2028.10 Under these assumptions, their expenditure could grow by an average of 5 per cent in 2026–2028, which would correspond to an expenditure increase of approximately EUR 250 million in 2028 relative to the Ministry of Finance forecast.

Counties II: For the 11 counties with accumulated deficits of 4 to 11 per cent relative to 2026 funding, expenditure could grow by an average of approximately 3 per cent per year over 2026–2028, approximately one percentage point less than in the Ministry of Finance forecast. In euro terms, this would correspond to consolidation of approximately EUR 350 million over three years relative to the Ministry of Finance forecast. These counties are most likely to be those that would meet the conditions for extending the deficit-covering period to either 2027 or 2028. The precise consolidation required of these counties thus also depends on the length of the extension granted. The consolidation requirement presented in the table for these counties can, however, be considered broadly realistic. These counties account for nearly half of the total WSC finances, so their expenditure development is of great significance for public finances as a whole.

Counties III: The five counties with accumulated deficits of 13 to 17 per cent relative to 2026 funding would need to keep their nominal annual expenditure growth at an average of 1 per cent over 2026–2028 in order to cover their deficits by the end of 2028. This expenditure growth rate would, for these counties, correspond to approximately EUR 400 million in lower expenditure in 2028 compared to the Ministry of Finance forecast. Some of these counties could meet the conditions for an extension of the deficit-covering period. However, covering deficits even by the end of 2028 may prove too demanding a target for some of these counties. The Government may therefore need to initiate assessment procedures also with some counties in this group.

Counties IV: The three counties in the weakest financial position would need to cut their expenditure in nominal terms by an average of just over 2 per cent annually over 2026–2028 in order to cover their deficits by the end of 2028. In euro terms, this would correspond to consolidation of EUR 500 million relative to the Ministry of Finance baseline forecast in 2028. In practice, however, these counties do not need to aim for such tight consolidation, as the government has already initiated assessment procedures with them. In simplified terms, the assessment procedure means that the fiscal consolidation of a WSC is determined in an assessment group established for the purpose. The consolidation timeline for these counties is thus assessed on a case-by-case basis.

The illustrative calculation presented above demonstrates how the scale of the required consolidation varies between counties in different financial positions, if all counties were to aim to cover their deficits by the end of 2028 at the latest. A few WSCs are likely to achieve a balanced financial position already during 2026, and these counties would even have room for expenditure increases. For the majority of counties, the additional time until the end of 2028 made available by the proposed legislative amendment should be sufficient to cover their deficits. However, it appears likely that for some counties, even the two-year extension will not be sufficient for achieving the necessary spending cuts.

The illustrative calculation uses financial statement forecast data for 2025. As noted above, the financial statement estimates reported in January 2026 indicate that the combined result of the WSCs would be better than the forecast data suggested. According to the estimate data, the 2025 result improved particularly for Helsinki, Vantaa-Kerava, Varsinais-Suomi and Länsi-Uusimaa. These counties in particular would have scope for larger expenditure increases than the maximum expenditure growth presented in Table 3.2.1. For the counties in the weakest financial position, the financial statement estimates do not indicate a significant change, meaning that the updated data would not materially alter the consolidation pressure presented in Table 3.2.1 for these counties. If the final 2025 financial statements confirm the developments indicated by the estimate data, the divergence between counties will be even more pronounced than presented here.

3.3 Needs-based allocation of funding

Central government funding for the wellbeing services counties is allocated on the basis of calculated factors. Approximately 80% of funding is allocated on the basis of county-specific health and social care service need. The calculation of service need is described in more detail in Text Box 3.1. Approximately 13% of funding is allocated on the basis of the county’s population. Other factors determining the allocation of funding include the share of foreign-language speakers, with a weight of approximately 2%, and the share of bilingual residents, with a weight of approximately 0.5%. In addition, county-specific transitional equalisation additions or deductions are applied to the county-specific imputed funding. These are calculated by comparing the combined 2022 expenditure of the municipalities in each county’s area with the county’s imputed funding at 2022 levels.

Development of the needs-based allocation of funding

The Finnish Institute for Health and Welfare (THL) calculates county-specific need coefficients annually on the basis of the most recent data on the use of services, such as diagnosis data collected by the counties and other morbidity data. Funding should thereby reflect changes in county-specific service need as accurately as possible. In counties where there has been an increase in (diagnosed/recorded) morbidity, funding rises to match the increased service need. However, the allocation of funding based on estimated service need is a zero-sum game between counties: funding correspondingly decreases in other counties if their morbidity levels have not changed.

In practice, however, diagnosis recording practices have varied across counties, and the data used by THL have also been affected by problems related to the transfer of diagnosis records and information systems. Some of the problems with the diagnosis data stem from the differing or deficient recording practices of municipalities, and the counties have sought to rectify these problems.11 As a consequence of problems related to diagnosis recording and data transmission, changes in county-specific need coefficients have not necessarily reflected changes in actual service need. Unforeseen changes in estimated service need and, consequently, in funding also complicate the counties’ financial planning. In addition, diagnosis-based funding creates a financial incentive to record certain types of diagnoses with a low threshold and, conversely, to economise on preventive services.

Problems associated with the assessment of service need could be significantly alleviated by discontinuing the use of morbidity data in the determination of county-specific service need. County-specific service need could be calculated more simply on the basis of population structure and certain socioeconomic factors.12 The advantage of such a model compared to the current one would be that the differing recording practices of counties and problems related to information systems would not affect the assessment of service need. As funding would no longer be based to a large extent on disease diagnoses, counties would have a clear incentive and opportunity to invest in disease prevention. Funding would also be more predictable than under the current model.

THL updates the need-factor model at least every four years, as required by law. In its most recent report on the update of the need-factor model (Holster et al., 2025), THL has calculated county-specific need coefficients using several alternative model specifications, one of which is based solely on population structure and certain socioeconomic factors. Although the addition of need factors slightly increases the models’ explanatory power at the individual level,13 a demographic model nevertheless produces, according to THL’s calculations, very similar results at the county level as the current model. In other words, although morbidity data naturally predict individual-level service need, their contribution to the assessment of county-level service need appears to be very limited. Given the potential ambiguities associated with diagnosis data, it is not clear that the current model produces even a marginally better estimate of actual service need across counties than a simpler model that disregards morbidity data.14